Prices extended losses

European gas prices extended losses yesterday, still pressured by weak demand and strong LNG supply. The drop in coal prices (-4.37% for API2 1st nearby prices,…

Equity markets continue to rally; the S&P 500 has erased half of its losses. US long rates stabilised as Fed members tried to put out the fire sparked by Jerome Powell’s statements last week: none of them are now suggesting that the Fed funds rate hike could be as high as 50bp in March and everyone seems to suggest that the market is right to expect 5 rate hikes this year.

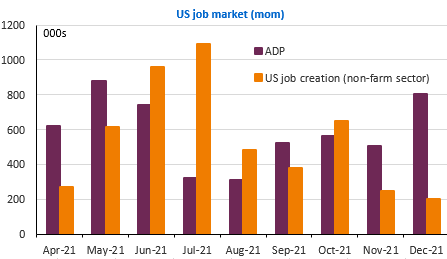

The private employment data compiled by ADP could reinforce this moderation trend in the short term as two elements suggest that it could be bad in January: on the one hand, it has deviated from the official data in recent months. On the other hand, the sharp rise in jobless claims suggests that the Omicron wave has had a real negative impact on the labour market. Indeed, the White House has been setting the stage for a poor January employment figure.

Eurozone inflation data will be watched closely ahead of the ECB meeting tomorrow. The available country data suggests that the decline was less than expected in January. The consensus is 4.4%, but analysts are leaning towards 4.8% after 5% in December. Our own estimate is 4.6%. The euro has already anticipated a stronger-than-expected figure and is rising towards USD 1.1270.