EUAs tracked the bearish energy complex

The surging wind output and strengthening solar and hydro generation weighted further on the Euporean power spot prices yesterday, although the rather strong demand, especially…

Concerns in Asia weighed on European markets yesterday and in Asia overnight with new restrictive measures adopted by Chinese authorities against tech companies as well as concerns over a possible debt restructuring of major property developer Evergrande. Wall Street had escaped the gloom thanks to a rebound in energy stocks in the wake of rising commodity prices. Industrial production in August and the New York Fed survey were also better than expected, while import price growth eased slightly.

Japan’s imports accelerated but exports slowed in August. It is difficult to draw solid conclusions from this as base effects remain strong.

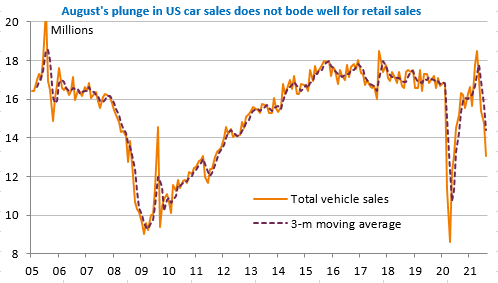

The markets are eagerly awaiting the day’s US figures and in particular retail sales: the sharp decline in car sales does not bode well, which could lead to a sharp downward revision of private consumption estimates in Q2 and consequently reinforce expectations of a status quo in Fed policy next week. In a well-known mechanism, the equity market could be happy with disappointing figures pulling rates down. It all depends on the extent of the disappointment.

The EUR/USD exchange rate remains close to 1.18.