What a day!

Spectacular reversal of the US equity markets yesterday, which lost more than 4% (for the Nasdaq) in the session and ended the day up. In…

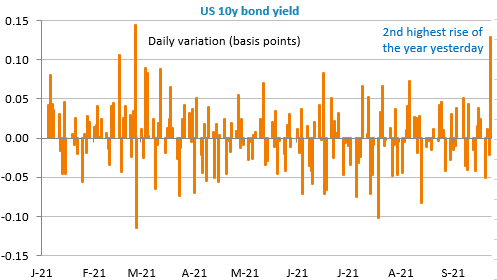

Rising equities, the second biggest rise of the year in bond yields and a falling dollar seem to suggest that it was more optimism about global growth (fuelled by continued strong PMI surveys in both Europe and the US) rather than just fear of inflation that dominated yesterday. However, these moves come just after Fed members came close to tilting towards a rate hike next year, on the day that the Bank of England chose to focus on inflationary risks rather than the Q3 slowdown and also on the day that the Norges Bank took the plunge and raised its key rates. This balance therefore appears fragile and it is not certain that risky assets can tolerate, without trembling, a further rise in long-term bond yields (+13bp on the US 10-year yesterday at 1.43%).

It is not the rate cut in Turkey as the inflation rate approaches 20% that will reverse the trend, as it seems to be solely dictated by political considerations, President Erdogan having promised this rate cut in September. The Turkish currency continues to plunge this morning to 8.8 against the USD.

The IFO survey in Germany will be the main economic report released today ahead of the general election this weekend with a very uncertain outcome. We will come back to this in the Weekly Economic Outlook later this morning. The dollar seems to be gaining some ground this morning (EUR/USD at 1.1735) while bond yields continue to increase.

Caution on Evergrande: there has been no communication on the subject, but some foreign investors report that they have not received the interest payment on the USD loan that was due yesterday.