First sanctions against Russia

The US, EU, UK and some of their allies have announced retaliatory measures against Russian interests after Vladimir Putin recognised the independence of the two breakaway republics…

European gas prices maintained their bullish momentum yesterday. Norwegian supply rebounded to 341 mm cm/day on average (compared to 331 mm cm/day on Wednesday) after the unplanned outage at the Oseberg field was fixed, but ongoing low Russian flows (stabilizing at 185 mm cm/day on average) and colder weather remained a concern. Asia JKM prices were slightly down (-1.87% on the spot, to €94.868/MWh; -0.16% for the February 2022 contract, to €102.960/MWh), which led to a narrowing of their premium against European prices.

After the meeting with coal mining companies which finally took place yesterday, Indonesia officials said discussions will be continued this Friday with a decision expected on the same day.

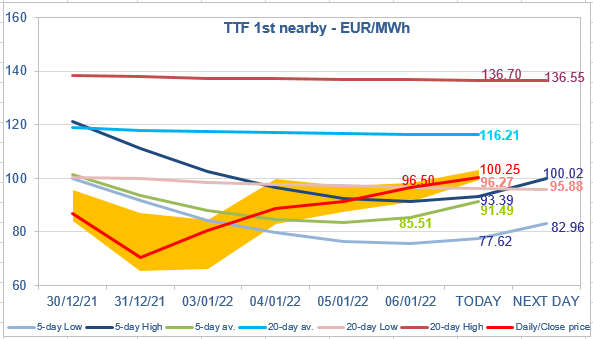

At the close, NBP ICE February 2022 prices increased by 11.750 p/th day-on-day (+5.26%), to 235.200 p/th. TTF ICE February 2022 prices were up by €4.98 (+5.44%), closing at €96.502/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.30 (+2.62%), closing at €50.753/MWh.

TTF ICE February 2022 prices closed yesterday almost at the 20-day Low level. They are rising again this morning, above this level, continuing their “normalization” process. Their new trading range seems now to be between the 20-day Low and the 20-day average. The decision on the Indonesia coal export ban could impact Asia LNG imports and decide in which part of this range they will trade.