Collapse at the prompt

The possibility of a coordinated SPR release is seriously denting the sentiment and upside risk in crude oil futures markets. Japan is now considering seriously an…

The Fed predictably raised its key rate by 75bp and warned that it could raise it again on a scale not seen since 1994 in July, but that it believed such action should be exceptional. Its growth and inflation forecasts were revised downwards and upwards respectively, but not excessively so, and the rate forecasts of the Fed members were set slightly below those of the markets. Conclusion: seriousness in the fight against inflation but no panic, no catastrophic forecast. This has rather reassured the markets since we can see an easing of bond rates (3.3% for the US 10-year, a rise in the equity markets and relative stability of the USD). A more detailed commentary on the Fed meeting was sent this morning. You can find it here.

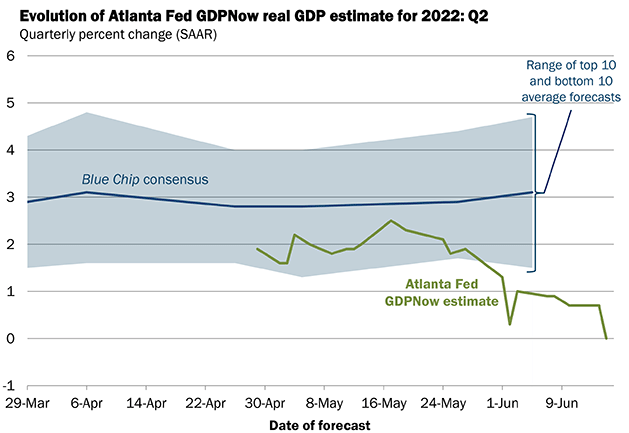

Prior to the Fed meeting, US retail sales figures disappointed with a 0.3% drop in July, mainly due to car sales. After these figures, the Atlanta Fed revised its Q2 GDP growth estimate to zero. Given that GDP already contracted in Q1, the US economy may in fact already be technically in recession, although domestic demand has so far held up well. The NAHB construction index also fell again.

Prior to these US figures, there was also a surprise ECB meeting and one could say that it was much ado about nothing: to defend sovereign bonds whose yields are soaring (because investors are selling them), the ECB will adjust the reinvestment of maturing bonds in its portfolio. But how? We don’t know. It will also develop a tool to deal more generally with bond market tensions in the euro area. What might this look like? When might it be due? A mystery. One can only be surprised (and cautious) at the sharp easing of southern bond yields that followed this announcement, as the reallocation of maturing bonds was already well anticipated by the market. The fairly sharp fall in the EUR/USD exchange rate below 1.04 shows that the foreign exchange market did not have the same view of this event.

On the agenda today, central banks again with the Bank of England meeting this time: the consensus is for a 25bp base rate hike, but there is a risk of a 50bp increase in the current context. Figures also from the US: construction activity, Philadelphia index and jobless claims.