Energy markets shaken up by tight supply

The EnergyScan team held its quarterly webinar covering key trends and events on energy markets. In this webinar, our experts addressed the following topics, with…

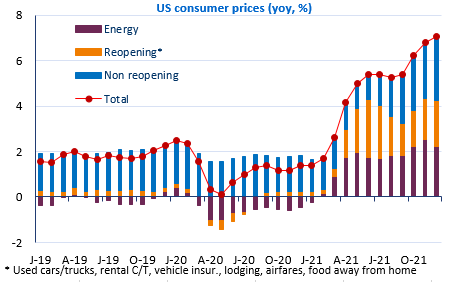

As expected, the US inflation rate reached 7% in December. The core inflation rate accelerated slightly more than expected to 5.5%. Whatever the measures of underlying inflation (they have multiplied in recent months in order to isolate the impact of the health crisis), the observation is always the same: structural forces are at work and the inflationary phenomenon is anything but transitory. If we break down the inflation rate into three components: energy, sectors whose prices have risen as a result of the crisis, and the others, it is this last component that prevails and explains nearly 40% of the 7%. It should also be noted that the energy effect has begun to diminish.

The markets’ reaction was muted, with long rates even falling initially and the equity market benefiting. The main impact was on the USD, which recorded its biggest daily drop since May 2021 (EUR/USD now above 1.1450, a two-month high)). All this seems to mean that the market considers that the Fed’s monetary tightening is perfectly anticipated from now on, i.e. between 3 and 4 rate hikes in 2022. However, this is far from certain. We believe that inflation could remain above 6% for most of the first half of the year and could end the year above 4%. The Fed will be under pressure to do more.

Today we will be watching US producer prices and jobless claims as well as Lael Brainard’s Senate hearing for the Fed’s n°2 position. Given that she is probably the mastermind behind the Fed’s strategic shift (in the summer of 2020) towards more inflation, it could be quite tense.