Inflationary risk still not taken seriously enough

The rise in the US inflation rate to 5.4% and the maintenance of core inflation at 4% in September reinforce the feeling that this transitory phenomenon linked to…

The FOMC Meeting Minutes unveiled details over a significant balance sheet reduction set to start as soon as next month with bond sales up to $95bn per month to cool the hottest inflation in four decades. The market impact was relatively limited as the US 10-y treasury yield briefly jumped to 2.66% before retreating towards 2.55% but its spread to the 2-y rate widened to a 2-week high.

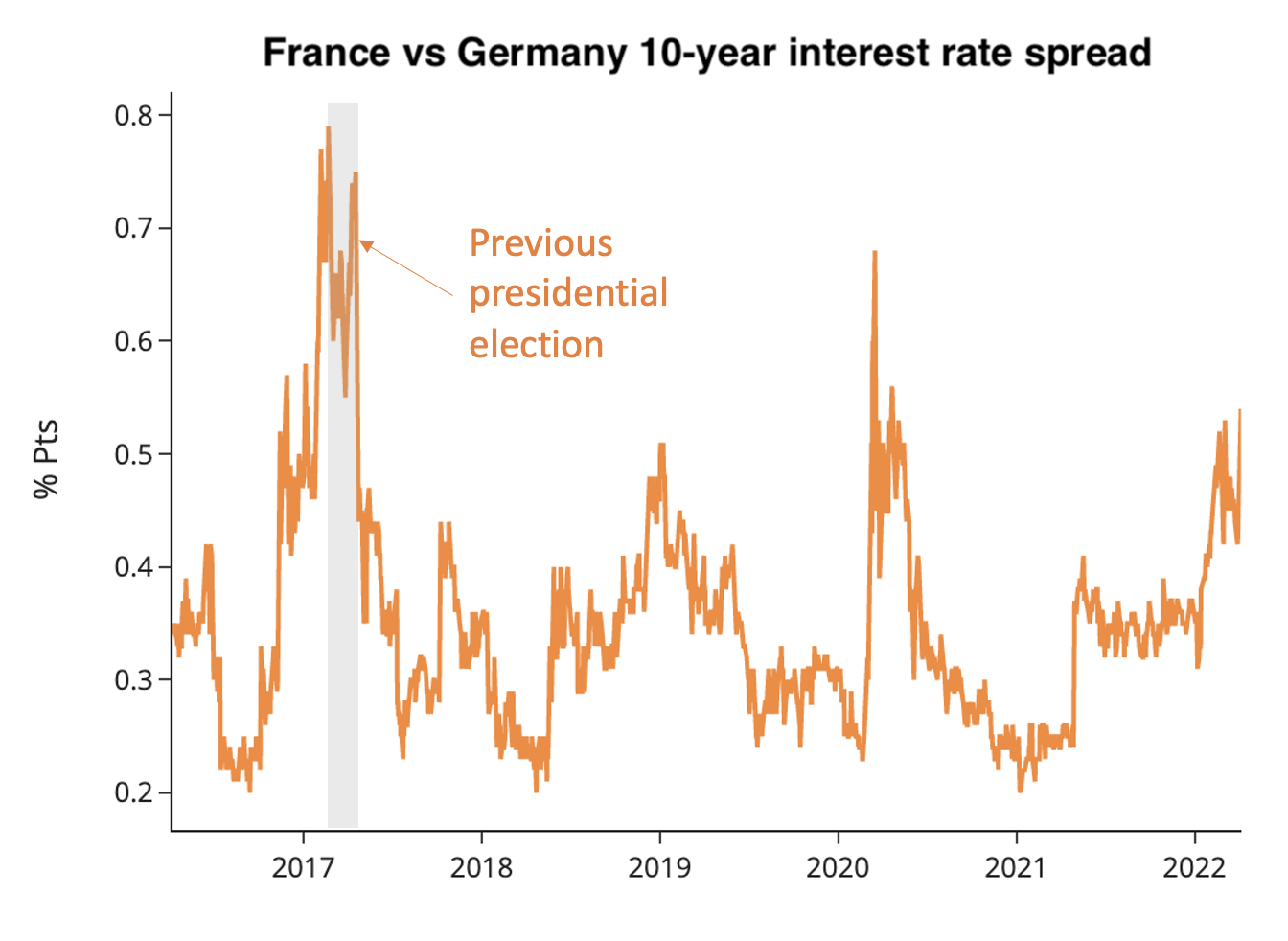

The upcoming French presidential election is pushing the 10-year French interest rate at a widening premium to the German Bund as recent polls showed a tightening spread between President Macron and the far-right candidate Marine Le Pen. The interest rate spread is not as high as it was in 2017 but recent moves show growing concerns among market players.

In Germany, industrial production grew by a mere 0.2% m-o-m in February 2022 despite lingering supply chain constraints, in line with the market consensus but well below January figures at 2.7% which confirms the economic slowdown ongoing.

On the agenda today, the release of retail sales in the Euro Zone should confirm the rebound in services activity following the loosening of COVID constraints.