Crude prices rally, supported by product markets

Brent prompt futures reached 59 $/b on early Thursday, despite a rally in the dollar as global inventories dwindled and OPEC+ member were renewing their commitments…

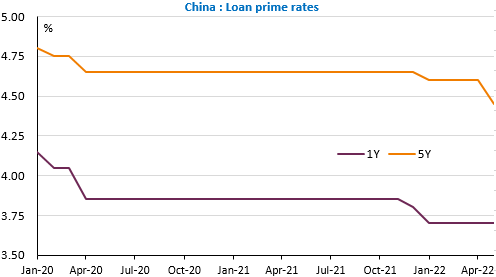

The yo-yoing continues on the markets: after a new decline in the equity markets yesterday and a sharp drop in long term rates (10 years US at 2.86% this morning), the trend was strongly reversed in Asia after Chinese banks lowered by 15bp the 5-year credit rate from 4.6% to 4.45%. The previous cut (-5bp) was in January and before that the last cuts were in the spring of 2020. Should we be happy about this as it will support the housing market or should we be concerned that the economic situation must be really serious for this decision to have been taken, which was already evident after the very poor activity figures in April? Unlike previous major economic downturns, the Chinese authorities have so far not pulled the credit lever to steer the property market to a soft landing in parallel. At this stage, we interpret this fairly sharp drop in lending rates as a parenthesis rather than a real change in strategy. At the same time, the People’s Bank of China released statistics showing property credit growth at its lowest since the series began in 2009 and a continued fall in transactions (obviously given the lockdown measures in major cities).

Yesterday’s decline in US existing home sales went unnoticed but it does seem to confirm the impact of rate hikes on the market. Similarly, the leading indicator fell, mainly due to the rise in jobless claims, confirmed by the statistics published yesterday (218k). It should also be noted that, like the New York index, the Philadelphia Fed index fell in May. Japan’s core inflation rate (excluding food) rose to 2.1%, but the rate excluding food and energy remains very low at 0.8%. This is not enough to bring the BoJ out of its “isolationism”. Retail sales rose strongly in the UK in April (+1.4% mom), despite a drop in consumer confidence to its lowest level ever. Producer prices continued to accelerate in Germany to +33.5% yoy. Monetary tightening is more important than ever in the UK and the Eurozone.

Economic calendar almost empty today. The EUR/USD exchange rate continued to rise towards 1.06.