China taps into its reserves to counter rising prices

The price of crude oil continues to be quite volatile without finding a real trend: yesterday it exceeded $73/b before dipping below $71/b and then…

European gas prices maintained their uptrend overall yesterday, supported by the additional rise in coal prices: +3.20% for API2 1st nearby prices; +3.04% for Cal 2023 prices. (More details are available in the Gas & Coal Weekly Report published yesterday.)

Norwegian flows weakened significantly yesterday, to 321 mm cm/day on average, compared to 337 mm cm/day on Wednesday, due to planned maintenance works. On their side, Russian flows remained stable, averaging 260 mm cm/day.

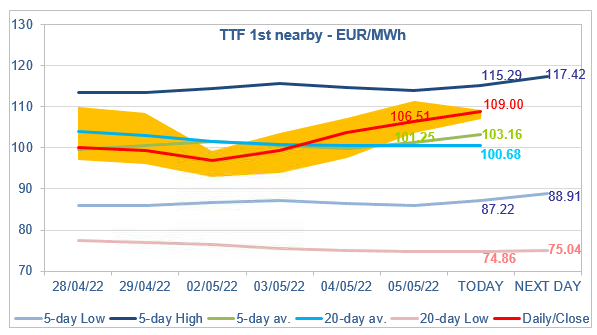

At the close, NBP ICE June 2022 prices increased by 7.030 p/th (+4.42%), to 166.230 p/th. TTF ICE June 2022 prices were up by €2.69 (+2.59%), closing at €106.508/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €2.38 (+2.87%), closing at €85.368/MWh.

In Asia, JKM spot prices increased by 2.03%, to €76.489/MWh; June 2022 prices increased by 1.21%, to €78.166/MWh.

The additional rise in coal prices pulled the maximum coal switching level to 102.37/MWh yesterday (up from 99.44/MWh on Wednesday), which continued to offer upside potential to TTF ICE June 2022 prices. Prices are up again this morning. The 5-day average, which is close to the maximum coal switching level, is now a strong support level. For the bulls, the 5-day High (115.29/MWh for today) seems to be an achievable target in the very short term.