US 10-year yield closes in on 2%

The US 10-year Treasury yield rose above 1.96% yesterday before easing slightly. It has not crossed 2% since July 2019; perhaps tomorrow when the January US inflation…

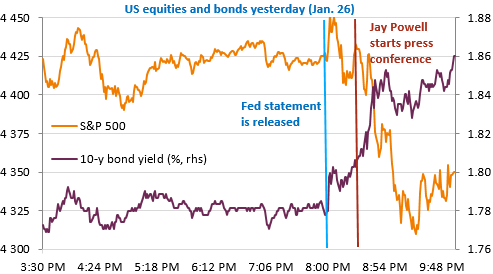

The Fed statement confirmed market expectations of a very likely rate hike in March and a process of reducing the size of the Fed’s balance sheet to follow. Until then, rates were rising without excess and the equity market was holding its gains.

It was when Jerome Powell started his press conference that everything went wrong: he did not give much more information but highlighted the differences with previous episodes of post financial crisis monetary tightening and the risks that inflation would not fall as expected and that the Fed would be forced to tighten policy much harder and faster than the market expected. The result is evident in the chart below.

More details in the News we sent yesterday evening. As a reminder, we also explained why the market was too optimistic in this report sent on Tuesday.

The Asian markets confirmed the trend: the day looks rough on the markets. The USD is also strengthening significantly to 1.12 against the euro. The day’s economic agenda is heavy with the publication of the first estimate of US GDP growth for Q4 2021, jobless claims and durable goods orders for December.