Oil markets react to stalled Hormuz traffic

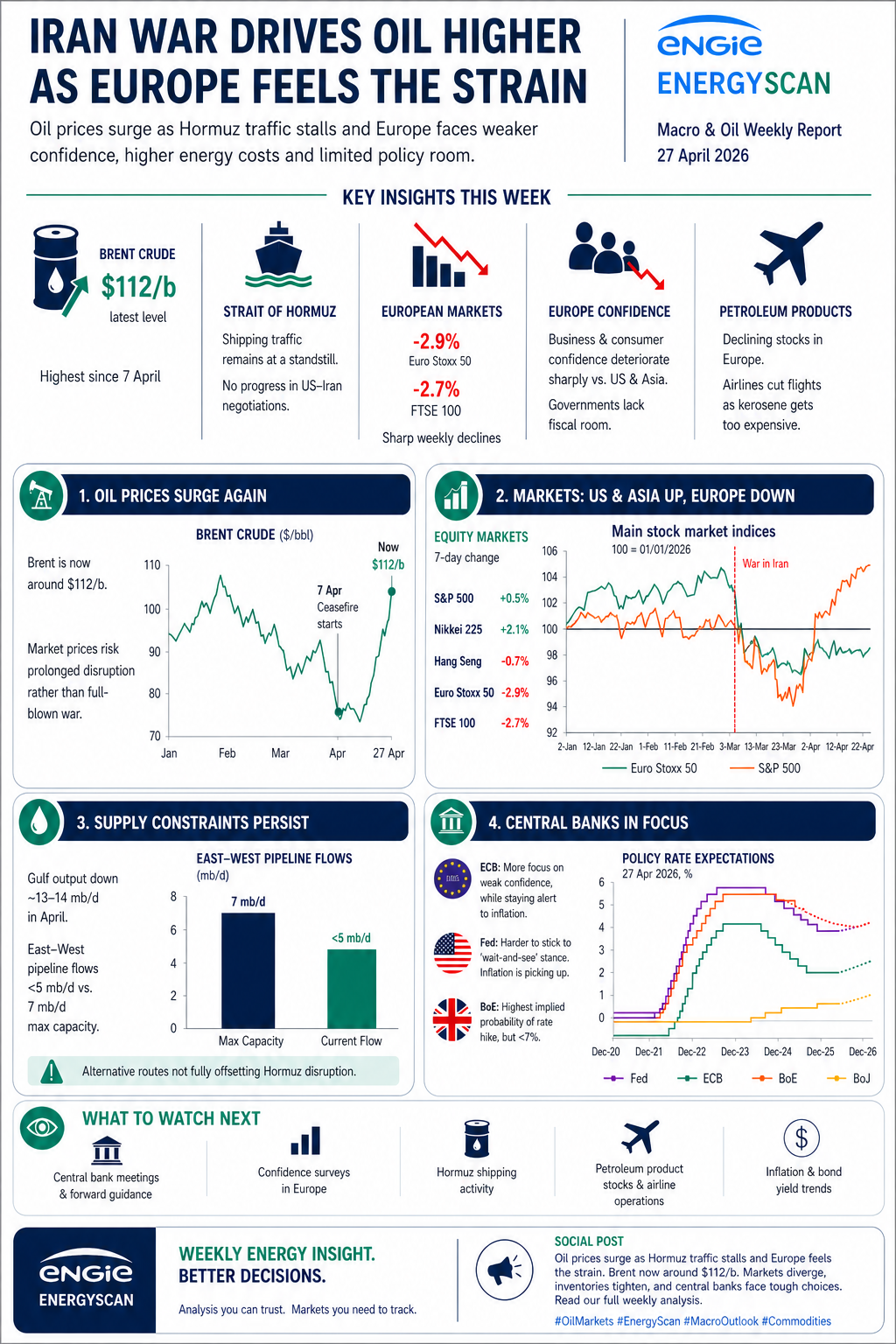

Brent crude has rebounded sharply as the situation around the Strait of Hormuz remains unresolved. On 17 April, Brent had fallen to $86.09/b following statements from Iranian authorities suggesting a reopening of the Strait. However, the US maintained its blockade of Iranian ports, and the Strait closed again almost immediately.

Shipping traffic has since remained highly restricted, with even fewer ships allowed through in recent days. In the report, Brent was already at $105.33/b, up $15/b over the week. Since then, oil prices have moved even higher, with Brent now around $112/b, reflecting continued disruption in the Strait of Hormuz and the lack of progress in US–Iran relations.

The market is therefore pricing two simultaneous risks. On the one hand, it does not appear to expect a full resumption of conflict, which would likely bring further damage to oil infrastructure in Iran and the Gulf states. On the other hand, it is becoming increasingly sceptical about a rapid return to normal market conditions.

Gulf output losses and pipeline constraints add pressure

Supply concerns are intensifying. Estimates of the drop in Gulf countries’ oil output in April have risen to around 13–14 mb/d. At the same time, flows through the East-West pipeline, which transports Saudi oil to the Red Sea, appear to be below capacity.

According to the report, less than 5 mb/d has been flowing through the pipeline, compared with a maximum capacity of 7 mb/d. This reinforces the sense that alternative export routes are not fully offsetting the disruption around the Strait of Hormuz.

For energy market participants, this means that the current oil price rally is not only driven by geopolitical headlines. It is also supported by concrete constraints on shipping, production and regional export logistics.

Europe faces early signs of economic stress

The impact is already visible in European financial markets. While US equity markets continued to rise, supported in particular by technology stocks, European markets moved in the opposite direction. The Euro Stoxx 50 fell by nearly 3%, while London’s FTSE 100 also dropped sharply.

Confidence indicators published last week showed a clear deterioration in Europe, affecting both businesses and consumers. This weakness stands in contrast with the United States and Asia, despite Asia’s dependence on imports from Gulf states.

Europe’s vulnerability is also linked to limited policy room. Governments face higher debt levels than in previous crises, reducing their ability to shield consumers and businesses from rising energy costs. Monetary policy is also constrained by inflationary pressure, making it more difficult to respond with rate cuts.

Petroleum product stocks become a key concern

Beyond crude oil, petroleum product stocks are becoming increasingly important. In Europe, declining product inventories are causing concern. Although the official communication remains reassuring on petrol, several airlines, including Lufthansa, KLM and SAS, have already announced plans to reduce scheduled flights over the coming months.

The report highlights two reasons: kerosene has become too expensive, and supplies need to be conserved ahead of expected higher demand in the summer. This indicates that the energy shock is already moving beyond financial markets and into operational decisions across transport and aviation.

In the United States, weekly data also show a decline in petroleum product stocks, mainly due to a sharp rise in exports. However, crude oil inventories remain comfortable, and shale producers appear determined not to increase output, viewing the price rise as temporary.

Central banks face a more difficult policy environment

The week ahead will be important for monetary policy, with major central bank meetings and key economic indicators scheduled. No change in interest rates is expected. However, central banks now have more data than they did at the beginning of the war.

The ECB is expected to pay closer attention to the sharp deterioration in confidence surveys, while still keeping inflation risks in focus. The Fed, meanwhile, may find it harder to maintain the same wait-and-see stance it adopted in March, as US indicators remain strong and inflation is picking up.

For energy professionals, central bank communication will matter because it may influence currencies, bond yields, demand expectations and broader risk appetite.

Key takeaways

- Brent has moved higher again, reaching around $112/b as the Strait of Hormuz remains disrupted and US-Iran negotiations show no progress.

- Europe is already showing signs of stress, with weaker markets, deteriorating confidence and limited fiscal flexibility.

- Petroleum product stocks, especially in Europe, are becoming a growing concern for transport and aviation sectors.

Conclusion

The Iran war is increasingly shaping energy and macroeconomic conditions. Oil markets are pricing prolonged disruption, with Brent now around $112/b, while Europe is already feeling the pressure through weaker confidence, falling equity markets and concerns over petroleum product availability. For market participants, the key issue is no longer only whether the conflict escalates, but how long disrupted flows and elevated energy costs can persist.

keywords

Iran war, oil prices, Brent crude, Strait of Hormuz, European markets, energy costs, inflation, petroleum stocks