OPEC discipline boost prices

Brent prompt month futures hiked higher, at 56.9 $/b on early Tuesday, as various third party agencies reported improved production compliance from OPEC members. Industry sources…

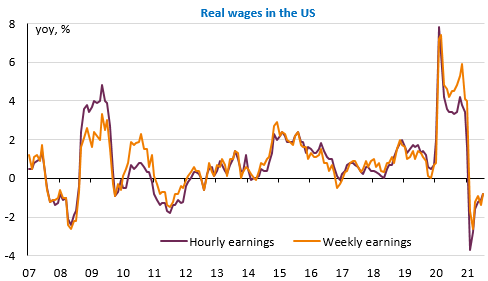

The rise in the US inflation rate to 5.4% and the maintenance of core inflation at 4% in September reinforce the feeling that this transitory phenomenon linked to the Covid crisis… is bound to last. This is also what Fed members fear from the minutes of their last meeting. They confirmed that the announcement of a reduction in securities purchases would probably come at the next meeting in early November, and that this reduction would take place at a rate of around $15bn per month. But they also revealed that: “Most participants saw inflation risks as weighted to the upside because of concerns that supply disruptions and labor shortages might last longer and might have larger or more persistent effects on prices and wages than they currently assumed”. In this respect, the price surge is causing a contraction in real wages: -0.8% yoy for both hourly and weekly wages.

What else can we expect but an acceleration in wages if companies are facing particularly strong recruitment difficulties?

In China, producer prices accelerated to +10.7% year-on-year in September while consumer prices rose by only 0.7% over the same period. This implies the strongest downward pressure on corporate margins in almost 30 years. The fact that the authorities have allowed the electricity companies to pass on the increase in the cost of their inputs will result in an acceleration of consumer prices and export prices which will reinforce the upward factors at the global level.

In this context, we can only be surprised that long-term bond yields eased slightly yesterday (the US 10-year is at 1.55%), as if the bond market was already anticipating the coming economic slowdown. But this seems premature and, above all, inconsistent with the optimism still displayed by the equity markets. Furthermore, the dollar is falling against the euro, towards 1.16, another signal of confidence sent by the market.

However, bad news on the inflation front is still expected today with the release of US producer prices.