Markets heading for the French presidential election

We are currently facing an IT issue. Our team is working on it. We apologize for the inconvenience. Financial markets continued to digest the massive…

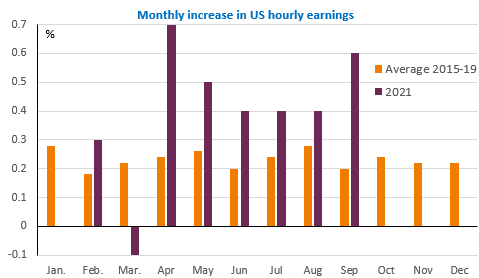

The US job report for September was not as bad as the weak job creation might suggest, as we explained here on Friday. The acceleration of wages is obvious and cannot leave the Fed indifferent: it should announce the beginning of the reduction of its asset purchases on 3 November. The markets will then focus on the timing of the rate hike, which should increase the upward pressure on bond yield. Indeed, the 10-year rate has risen above 1.6%, despite the employment figures.

In the UK, bond yields are soaring: the 10-year has climbed 60bp in less than two months. The markets are now expecting monetary tightening before the end of the year. Inflationary pressures are not about to abate with the disruption of production and distribution chains (amplified in the UK by the Brexit) and commodity prices still rising.

US markets are closed (Columbus Day), which could give European markets some breathing space today. The EUR/USD exchange rate is up slightly to 1.1580, but this rebound does not appear to be solid.