Margins collapse

Crude prices continued to weaken on Wednesday despite the dollar edging lower, as the physical market’s weakness filtered through the futures’ market. Weak physical crude…

Financial markets were still dominated by pessimism yesterday, as evidenced by the sharp rise in the US dollar, with the exchange rate against the euro plunging to 1.0354, close to the January 2017 low. The trend seems to have reversed with a new interview with the Fed Chairman. It seems to be a replay of last week’s scene, when equity markets rebounded only because Jerome Powell seemed to rule out a 75bp rate hike, before falling back heavily in the following days. The US producer price figures released yesterday delivered much the same message as the consumer price figures: a slowdown in April but less than expected: +11% yoy. The Fed will therefore continue its monetary tightening with a 50bp increase in the Fed funds rate in June.

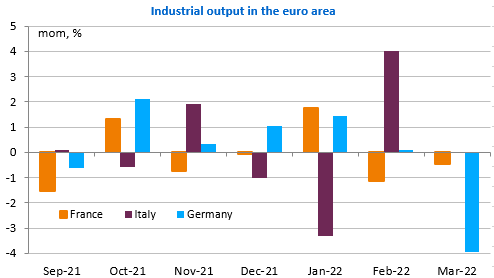

In the euro area, the ECB should also start raising interest rates in July due to inflationary pressures and despite the risks of a contraction in activity in the current quarter. Industrial activity has already fallen sharply in March, especially in Germany (by almost 4% m/m). Eurozone figures will be published this morning. Otherwise, we will keep an eye on some US figures: import prices this time and the University of Michigan’s consumer survey, with a particular focus on inflation expectations of course.