Carbon options’ expiry continued to maintained prices near 80€/t

Except in France where prices inched down on expectations of weaker demand, the European power spot prices slightly rose yesterday, buoyed by forecasts of dropping…

Growth concerns continue to drive the markets: after a strong rebound, the US equity indices almost all ended lower yesterday, but a final surge saw the S&P and Nasdaq rise slightly, but not the Dow Jones. The US 10-year yield fell back below 3% and the USD strengthened a little, confirming risk aversion. The rebound in the Asian markets comes from information on a drop in Covid cases in China, which suggests a gradual recovery in activity.

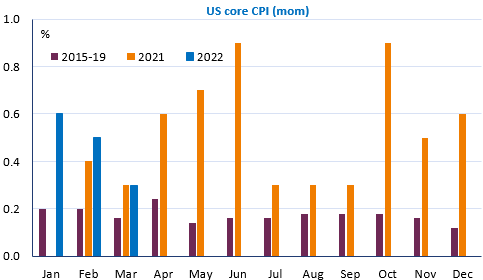

The event of the day and of the week is the release of the US inflation figures for April. This is an event because a drop is expected (from +8.5% to +8.1% yoy) and if this is indeed the case, it is reasonable to think that the inflation peak was reached in March. We discussed this in the Macro & Oil Weekly Report published on Monday. The graph below also illustrates that the trend in core inflation already seems to be slowing down since the beginning of the year, especially in goods prices which had soared with the Covid epidemic. With the favourable base effect on energy prices pulling the inflation rate down, the markets will probably focus more and more on core inflation and precisely watch if the strong wage increases or the foreseeable acceleration of rents in the wake of real estate prices push up the prices of services and prevent or slow the decline. This will also be a crucial question for the Fed.