Prices maintained their short term downtrend

European gas prices dropped significantly yesterday, still pressured by above-normal temperatures and more comfortable supply. Norwegian flows rebounded to 337 mm cm/day on average yesterday,…

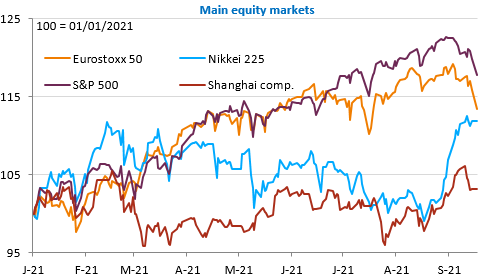

Equity markets suffered significant losses yesterday as they were caught up in the turmoil of the collapse of China’s Evergrande property developer. US indices did recover in the latter part of the session, a trend that was confirmed in Asia overnight, except in Japan where markets were closed yesterday. The consensus seems to be that the Chinese authorities will not risk another Lehman, but are determined not to back down this time when it comes to calming the property market. Ending property speculation seems to be a logical part of Xi Jinping’s broader strategy of “common prosperity”. There will therefore be consequences for financial actors and in particular foreign investors, but small savers should be preserved. On the other hand, the economic consequences are probably underestimated: real estate and construction represent nearly 30% of GDP.

As far as the Fed is concerned, which is meeting today and tomorrow, it is clear that the rise in risks on the markets can only encourage them to be prudent. It is worth noting, however, that US long-term bind yields hardly fell at all yesterday. Inflationary concerns remain very present.

Today, we have the OECD forecast update and the US construction data for August, but the markets will continue to be guided by the news about Evergrande and the caution before the Fed meeting.