Carbon prices hit new record prices on spiking gas market

If forecasts of surging wind pressured the German power spot prices yesterday, day-ahead prices elsewhere in NWEurope posted hefty gains amid a significant rise of…

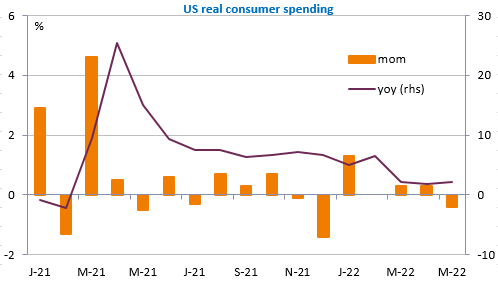

For the first time since the beginning of the year, US consumer spending contracted in real terms (deflated for inflation) in May, amplifying recession fears and the downward correction in equity markets.

Overall, the S&P 500 fell by 20.8% in the first half of the year, the Nasdaq by 30% and in Europe, the Euro Stoxx 50 by 19.8%. Long term yields also continued to fall, with the US 10 year falling back below 3%, while they fell even more sharply in Europe and the EUR/USD exchange rate broke through the 1.04 support (before rebounding to 1.0460). But the core PCE, the Fed’s preferred inflation indicator, also slowed for the 3rd consecutive month, counteracting the impact of the hawkish statements by central bankers in Sintra. The markets are hoping that these signs of slowing demand and inflation will be enough to slow down the Fed’s monetary tightening.

Another busy day today: the Tankan, the BoJ’s quarterly survey, gave mixed results showing both the negative impact of the China lockdown on Q2 activity and a slight improvement in the outlook for Q3. The Chinese Caixin PMI confirmed the improvement in the manufacturing sector with a sharp rise from 48.1 to 51.7. But this is a special case and the manufacturing PMIs in Europe and the US should rather highlight a clear slowdown in activity and it seems to us in particular that the consensus is too high for the ISM in view of the rather sharp decline in regional indices, such as the Chicago PMI yesterday (-4.3 points). That leaves the Eurozone inflation figures, but the risks of disappointment seem limited by the decline in Germany: the inflation rate may have increased again (8.1% in May), but less than initially expected.