Euro at 5-year low against USD

1.0616 at the time of writing, possibly lower by the time of publication. The EUR/USD exchange rate has sunk below its 2020 lows. You have to go…

We spent the week noting the curious decline in bond yields while the US figures were frankly good. If they rebounded yesterday, it was not thanks to the first estimate of Q3 US GDP growth, which came in below consensus expectations (+2% annualized quarterly change), with inventories making a very large contribution to growth. Nevertheless, the outlook is improving as the pandemic subsides and the Fed is not expected to change its plans for next week as we pointed out yesterday.

The rebound in interest rates did come from the ECB meeting, as markets felt Ms. Lagarde was too timid to push back expectations of a rate hike as early as next year. While the ECB’s stance on the transitory nature of inflationary pressures has not changed, it now recognizes that they will be stronger than expected and will last longer. More details here.

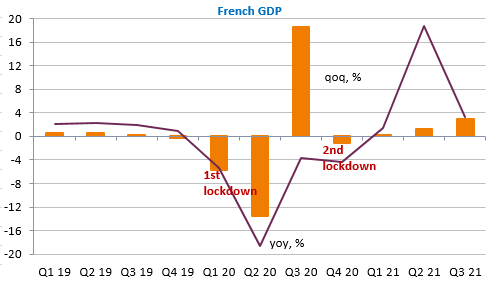

The US 10-year yield is back above 1.6% and the German Bund is back to -0.12%. It is mainly the peripheral markets of the euro zone that have suffered: the spread with Italy has widened by 9bp! The euro is also stronger against the USD at 1.1670 and could continue to strengthen given the day’s agenda. The euro area GDP is expected to rise sharply in Q3 (consensus +2.1% q/q non-annualized), especially after the excellent figures for France (+3%).

The euro area inflation is also expected to rise in October (consensus +3.7%) after yesterday’s data from Germany (+4.6%) and Spain (+5.5%).

A few indicators to watch in the US (consumption and prices in October, revised figures from the University of Michigan confidence survey and the Chicago area PMI) as well as a possible agreement on the Biden plans in the US Congress.