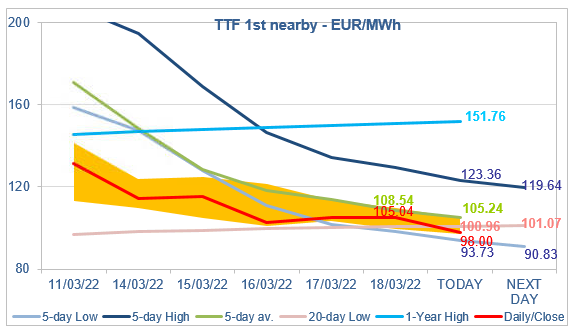

Prices torn between comfortable spot fundamentals and concerns on Russian supply

European spot gas prices dropped strongly on Friday, pressured by weak demand and ongoing strong LNG supply while pipeline flows remained stable (Norwegian flows at 320…