A calm end of the week for the energy markets

The European power spot prices for today slightly decreased compared to Friday, pressured by forecasts of higher solar and hydro production and slightly lower gas…

The decline in long term bond yields was accentuated yesterday, pulling the US 10 year down to 1.43%, mainly on the idea that Joe Biden might decide to replace Jerome Powell with Lael Brainard, the advocate of “infinite QE”. In reality, both have always voted exactly the same way at Fed meetings and a change in the head of the Fed would not be without risk. It is unlikely that Joe Biden would take it up, especially for potentially favouring a more lax policy towards inflation that could hurt him in the mid-term elections.

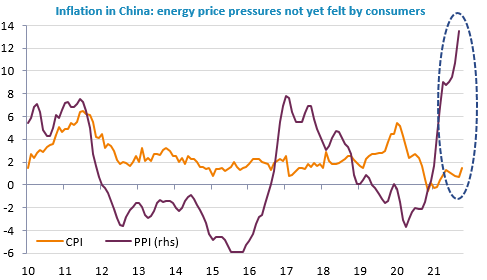

Bond yields are rising a bit this morning. The NFIB survey confirmed the concomitant acceleration of prices and wages among small businesses in the US. Chinese producer prices soared in October to +13.5% yoy and the consequences are still to come for the consumer.

Finally, US inflation figures will be released today on the heels of yesterday’s producer prices. The inflation rate is expected to be close to 6% in October. Note that jobless claims will also be released today. This could reinforce the feeling that inflationary pressures are increasing and that the recent fall in bond yields is out of touch with reality.

The EUR/USD exchange rate rose above 1.16, before falling back to 1.1570. Still no clear trend.