Kazakh crude exports at risk

Crude prices soared past 82 $/b yesterday for the March ICE Brent contract, with March/April time spreads rallying strongly to 70 cents, as the political…

While the fighting in Ukraine is intensifying, financial markets seem to be calming down somewhat. Equity markets trimmed their losses in Europe yesterday, fell little in the US (with the Nasdaq even rising) and rose in Asia. One explanation is the sharp fall in long rates and even more so in real terms, as nominal rates fall while rising commodity prices reinforce inflation expectations. It is also likely that markets are now waiting to see how the military situation and the first impacts of economic sanctions on Russia will evolve. The rouble fell sharply yesterday, forcing the Russian Central Bank to raise its key rate to 20% and to implement capital controls, which are expected to be tightened. Switzerland has abandoned its neutrality by adopting the Western sanctions. Based on the transactions recorded by the BIS, it is estimated that a third of the wealth of Russian oligarchs could be blocked in Swiss bank accounts! Are the sanctions against Russia likely to turn public opinion in Russia against its leaders? Can they have collateral damage on Western companies and banks in the short term, especially after cutting off access to Swift for some Russian banks?

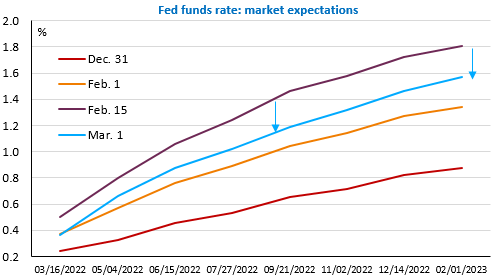

The final element is that the economic calendar is regaining some importance. Not so much with the manufacturing PMIs released today, but with the German inflation figures today and the Eurozone tomorrow, and most importantly, the Fed Chairman’s hearings before the US Congressional Banking Committees on Wednesday and Thursday, followed by the US jobs report on Friday. The market is now ruling out a 50bp rate hike by the Fed and sees only 5 hikes this year compared to nearly 7 a few days ago. Hasn’t it gone too fast? There are many factors to consider, which may explain the wait-and-see attitude at this stage.