EUAs continued to extend their sharp bullish trend

The power spot prices were mixed yesterday, up in Germany, Belgium and the Netherlands on forecasts of dropping wind output, but down in France as…

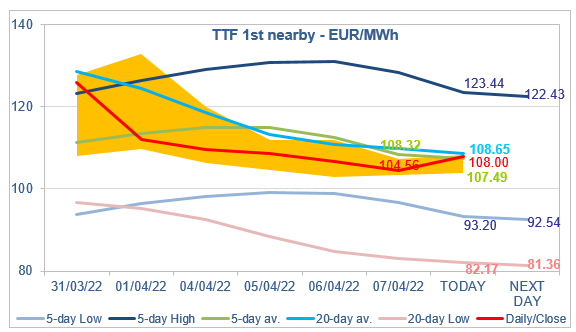

European gas prices weakened again yesterday, particularly on the spot and the near curve, still pressured by comfortable spot fundamentals overall despite slightly lower pipeline supply. Indeed, Russian flows were almost stable yesterday, averaging 260 mm cm/day, compared to 261 mm cm/day on Wednesday. Norwegian flows weakened to 320 mm cm/day on average, compared to 324 mm cm/day on Wednesday, impacted by outages at Gullfaks and Bacton Perenco.

Note that the European Parliament made yesterday a (non-binding) proposal for an immediate EU-wide full embargo on Russian energy imports, including natural gas.

At the close, NBP ICE May 2022 prices dropped by 5.930 p/th day-on-day (-2.48%), to 233.490 p/th. TTF ICE May 2022 prices were down by €2.23 (-2.09%), closing at €104.564/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 29 euro cents (-0.39%), closing at €74.903/MWh.

In Asia, JKM spot prices dropped by 3.92%, to €96.931/MWh; May 2022 prices dropped by 0.88%, to €103.826/MWh.

Coal prices weakened yesterday, pulling the maximum coal switching level down to €90/MWh. This offered the potential for lower TTF ICE May 2022 prices. However, their inability to drop to the 5-day Low (which would have brought them closer to the coal switching level) suggests that market participants consider the European gas balance is still too fragile. And indeed, the resilience in Asia JKM May 2022 prices (although prices from June are lower) is a risk for European LNG supply. With TTF prices trading this morning around their 5-day average and their 20-day average, we will know very soon if the bearish trend is confirmed or reversed.