US inflation rate hit a new 40-year high

The release of the US CPI figures showed a further acceleration in the inflation rate in March 2022 at 8.5% yoy, which was the largest year-on-year…

The US bond market was closed yesterday, bringing some calm after a sharp rise in yields last week that was not halted by the release of much lower than expected job creation figures. The equity markets are still down due to uncertainties in China (real estate, regulation, energy shortages and soaring costs) and ahead of a series of key US economic reports this week: inflation, retail sales, consumer confidence and Fed Minutes.

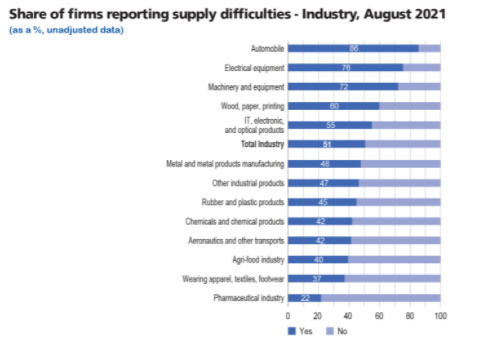

The Banque of France survey shows a deterioration of the business climate in September, mainly linked to supply difficulties in industry (particularly in the automotive sector) and rising costs. This situation is of course not unique to France.

To be followed today are the ZEW survey in Germany, the business climate for small businesses in the US (NFIB) and the IMF Outlook. The EUR/USD exchange rate is fairly stable, just above 1.1550.