Limited moves on financial markets

Financial markets are rather calm in general, with limited moves on equities, bonds and FX. The EUR/USD exchange rate has edged down but remains not…

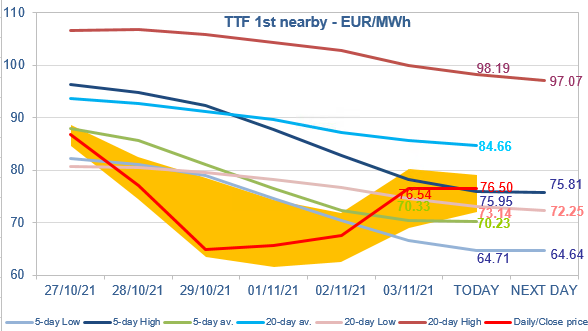

European gas prices continued their rebound yesterday, posting strong gains as they got support from the rise in Asia JKM prices (+7.15%, to €82.262/MWh, on the spot; +6.03%, to €96.266/MWh, for the December 2021 contract) and in parity prices with coal for power generation (thanks to the strong rise in API2 coal prices). They ignored the increase in pipeline supply. Indeed, Russian supply increased strongly yesterday, to 235 mm cm/day on average, compared to 217 mm cm/day on Tuesday, thanks to the additional rise in flows through Ukraine. Norwegian flows were also up, averaging 346 mm cm/day, compared to 340 mm cm/day on Tuesday.

At the close, NBP ICE December 2021 prices increased by 23.440 p/th day-on-day (+13.53%), to 196.720 p/th. TTF ICE December 2021 prices were up by €8.94 (+13.22%) at the close, to €76.542/MWh. On the far curve, TTF Cal 2022 prices were up by €3.89 (+8.45%), closing at €49.910/MWh, and widening the spread against the coal parity price (€33.103/MWh, +7.31%).

The rebound in TTF ICE December 2021 prices yesterday was finally bigger than we thought. Prices increased by the full potential allowed by the technical rebound, i.e. up the 5-day High. For the short-term downtrend not to be called into question, prices must fall now. Fundamentals, both in Europe and in Asia, justify this drop. In China, the (additional) moderate increase in coal prices suggests that the rebound is only technical, and anyway prices are still well above the supposed official preferred zone, which means their upside potential is limited. This morning, the 5-day High is effectively setting a resistance, paving the way for lower prices. However, in case of an unforeseen fundamental event, a break above this resistance level towards the 20-day average is a possibility.