Macro & Oil Report: Prospects for a rate cut in the US seriously shaken

Prospects for a rate cut in the US seriously shaken Macro & Oil #89 There are three main lessons to be learned from the past…

The fall seems to have stopped: the price of Brent had lost around $30/b in a week and even more if we consider the peak of $139/b reached briefly. For the past two days, it has been hovering around $100/b and is even showing signs of a rebound. It is true that hopes for peace in Ukraine are rising, but the sanctions against Russia will last and the containment measures in China may not be as strict as expected, thus reducing the negative impact on demand.

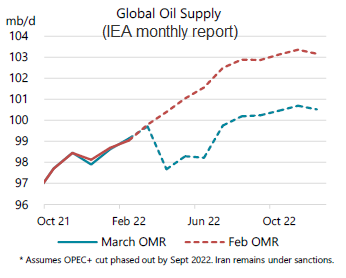

More importantly, initial estimates point to a significant decline in Russian oil exports to Europe, despite the calibration of sanctions to spare energy. Based on transactions since the beginning of the month and forecast to date, these exports could fall by 40mb, or 1.3mb/d according to Reuters. The IEA report released yesterday is even more alarming: the drop in exports would force Russia to reduce its production by 3mb/d as early as next month.

The IEA revised its oil demand forecast for this year sharply downwards due to the impact of higher prices, but at the same time lowered its non-OPEC supply forecast, including Russia, by 2.1mb, which is twice as much as the demand revision. As a result, the IEA estimates that the oil market could be in deficit over the next two quarters, whereas a surplus was expected. Libya, which is part of OPEC but not part of the OPEC+ agreement, yesterday called on OPEC to increase production.

The weekly EIA report showed a sharp rise in crude oil inventories but still no rise in production and a sharp decline in gasoline stocks. More details here.