Outright crude crashes

By falling below 80 $/b, ICE Brent front-month future declined by close to 4.5% within a day. Yet, front-month time spreads remained supported, at 127…

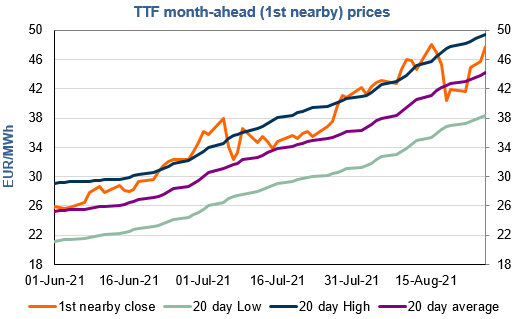

European gas prices increased strongly last Friday, supported by ongoing tight fundamentals (strong injection demand due to relatively weak stock levels while supply remains constrained) and short-covering for the last trading day of the September contract. The strong rise in Asia JKM prices (+5.28% on the spot, to €51.355/MWh) and in parity prices with coal for power generation (both coal and EUA prices were up) also helped to support the upward pressure.

On the pipeline supply side, Russian flows were almost stable last Friday, averaging 313 mm cm/day (compared to 312 mm cm/day on Thursday). By contrast, Norwegian flows were lower, averaging 307 mm cm/day (compared to 319 mm cm/day on Thursday), due to unplanned maintenance works.

At the close, NBP ICE September 2021 prices increased by 5.870 p/th day-on-day (+5.10%), to 120.970 p/th. TTF ICE September 2021 prices were up by 202 euro cents (+4.41%) at the close, to €47.806/MWh. On the far curve, TTF Cal 2022 prices were up by 73 euro cents (+2.30%), closing at €32.686/MWh, above the coal parity price (€31.909/MWh).

Tight fundamentals could continue to lend support to European gas prices today. But, after the strong increase of the previous sessions, profit taking by financial participants and technical resistances (€49.744/MWh on TTF October 2021 and €32.749/MWh on TTF Cal 2022) could contribute to limit gains.