Powell’s comments drive price lower

Oil prices fell yesterday: ICE Brent for July delivery closed at $111.93/b, making a -2% loss, while NYMEX WTI first nearby prices settled at $112.40/b,…

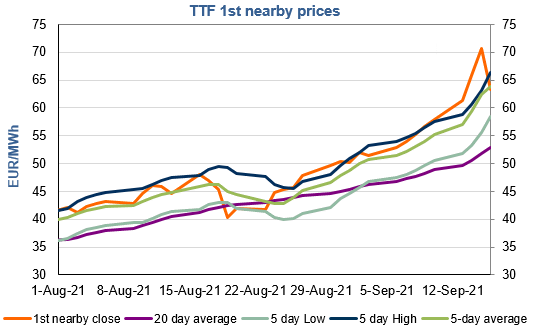

European gas prices dropped significantly yesterday, pressured by more comfortable pipeline supply and profit taking after the previous sessions’ strong gains. Russian flows were stable yesterday, averaging 318 mm cm/day, above the levels of end August (313 mm cm/day). Norwegian flows continued to rebound, to 288 mm cm/day on average (compared to 280 mm cm/day on Wednesday), as planned maintenance works ended.

Asia JKM prices (+2.63% on the spot, to €72.616/MWh) and parity prices with coal for power generation (both coal and EUA prices were down) sent mixed signals.

At the close, NBP ICE October 2021 prices dropped by 18.920 p/th day-on-day (-10.67%), to 158.380 p/th. TTF ICE October 2021 prices were down by €7.46 (-10.54%) at the close, to €63.251/MWh. On the far curve, TTF Cal 2022 prices were down by €2.69 (-6.39%), closing at €39.376/MWh, and increasing the spread against the coal parity price (€35.235/MWh).

Norwegian supply is up again this morning (to 297 mm cm/day). This could continue to exert downward pressure on European gas prices today. However, given the concerns on the fundamental situation (low stock levels, uncertainty on the commercial start date of Nord Stream 2), the drop should be limited, particularly as prices could benefit from technical supports (€63.055/MWh on TTF October 2021 and €39.571/MWh on TTF Cal 2022).