European spot and near curve prices strongly up

European spot and near curve gas prices increased strongly on Friday, supported by colder temperatures and lower renewable power generation. The tension in Asian markets…

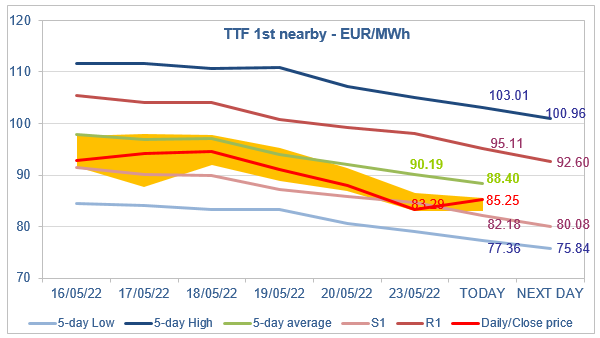

European spot gas prices increased yesterday, supported by lower pipeline supply. Indeed, Norwegian flows dropped to 305 mm cm/day on average (compared to 325 mm cm/day on Friday), due to an unplanned outage at the Troll gas field. Russian flows were also lower, averaging 208 mm cm/day, compared to 227 mm cm/day on Friday. By contrast, curve prices maintained their downtrend as the drop in coal prices (-5.83% for API2 1st nearby prices, -5.62% for Cal 2023 prices) did not provide any support.

Note that Gazprom suspended gas supplies to Gasum on 21 May after the Finnish company refused to pay for Russian gas in rubles. Gasum said previously that it will be able to supply all of its customers in coming months with gas imported via the Balticconnector with Estonia.

At the close, NBP ICE June 2022 prices dropped by 12.930 p/th (-8.74%), to 135.030 p/th, equivalent to €54.290/MWh. TTF ICE June 2022 prices were down by €4.61 (-5.25%), closing at €83.288/MWh. On the far curve, TTF ICE Cal 2023 prices dropped by €2.16 (-2.85%), closing at €73.552/MWh.

In Asia, JKM spot prices dropped by 0.97%, to €69.343/MWh; July 2022 prices increased by 2.30%, to €72.144/MWh; August 2022 prices dropped by 1.50%, to €74.075/MWh.

The drop in coal prices pulled the summer coal switching level to €70.77/MWh yesterday (down from €75.27/MWh on Friday), offering downside potential to TTF ICE June 2022 prices, which closed yesterday slightly below the S1 level. Prices are rebounding this morning. As we said yesterday, TTF prices are approaching the Asia JKM price levels, which means their downside potential is now limited.