EUAs hit new record on rising gas supply concerns

Expectations of stronger power demand and weaker French nuclear availability combined with higher fuels and carbon prices drove the European power spot prices above 130€/MWh…

After a strong start, European gas prices weakened by the close yesterday as the 30 mm cm/day of day-ahead transport capacity at Mallnow booked by Gazprom suggests Russian supply is likely to at least remain flat. The spread with Asia JKM prices (+2.43% on the spot, to €112.127/MWh; -1.24% for the January 2022 contract, to €108.195/MWh) widened slightly. On the spot pipeline supply side, Norwegian flows were slightly down yesterday, at 346 mm cm/day on average, compared to 349 mm cm/day on Monday. The same for Russian supply, which averaged 286 mm cm/day, compared to 285 mm cm/day on Monday.

At the close, NBP ICE January 2022 prices dropped by 1.450 p/th day-on-day (-0.61%), to 236.860 p/th. TTF ICE January 2022 prices were down by 93 euro cents (-1.00%) at the close, to €92.513/MWh. On the far curve, TTF Cal 2022 prices were down by 48 euro cents (-0.86%), closing at €55.256/MWh, with the spread against the coal parity price (€34.860/MWh, -3.88%) widening.

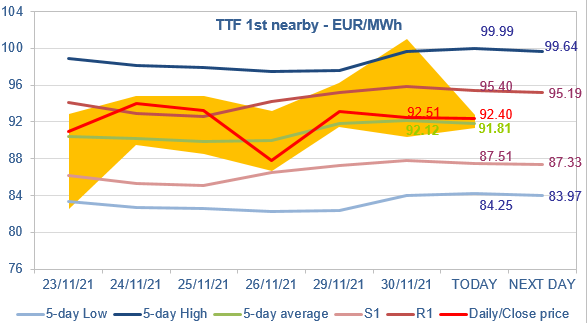

TTF ICE January 2022 prices challenged the 5-day High resistance yesterday before closing around the 5-day average. The volatility of the two last sessions comes mainly from the expiration of the December 2021 contract (with last minute buying). Prices could now stabilize within the S1-R1 range, with an upward bias due to the strong levels of Asia JKM prices.