European energy markets still in wait-and-see mode

Gas & Power Podcast #24 In this episode of the weekly EnergyScan podcast about the Gas&Power markets, Julien Hoarau tells us about how gas and…

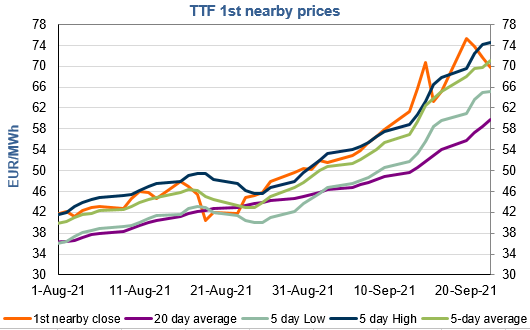

European gas spot and near curve prices continued to weaken yesterday, pressured once again by the drop in Asia JKM prices (-2.66% on the spot, to €76.018/MWh, -1.07% for the November 2021 contract, to €77.919/MWh) and profit taking. Prices on the far curve were more resilient, supported by the rise in parity prices with coal for power generation (thanks to the strong rise in coal prices).

On the pipeline supply side, Russian flows increased slightly yesterday, averaging 313 mm cm/day, compared to 311 mm cm/day on Wednesday. Norwegian flows were slightly up, to 289 mm cm/day on average, compared to 282 mm cm/day on Wednesday.

At the close, NBP ICE October 2021 prices dropped by 6.620 p/th day-on-day (-3.66%), to 174.490 p/th. TTF ICE October 2021 prices were down by 201 euro cents (-2.80%) at the close, to €69.684/MWh. On the far curve, TTF Cal 2022 prices were up by 25 euro cents (+0.58%), closing at €42.833/MWh, still significantly above the coal parity price (€36.332/MWh) although the spread narrowed.

Norwegian flows are significantly up this morning (to 319 mm cm/day) as the technical incident on the Aasta Hansteen gas field seems settled. This could exert downward pressure on European gas prices today. However, technical supports (€66.294/MWh on TTF October 2021 and €42.035/MWh on TTF Cal 2022) could contribute to limit losses.