Mixed price evolution

European gas prices were mixed yesterday. They received (moderate) support from lower pipeline supply. Indeed, Russian supply dropped to 210 mm cm/day on average yesterday,…

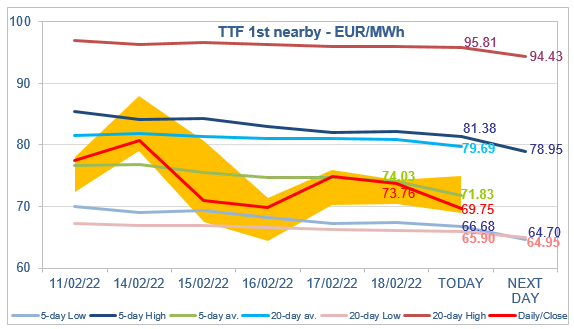

European gas prices weakened slightly on Friday as strong LNG supply and below-normal demand exerted downward pressure. Prices even ignored the strong drop in Norwegian supply (to 320 mm cm/day on average, compared to 341 mm cm/day on Thursday) due to an unplanned outage at the Nyhamna gas processing plant; on their side, Russian flows increased slightly to 186 mm cm/day on average, compared to 182 mm cm/day on Thursday. The moderation in Asia JKM prices (+0.04% on the spot, to €73.233/MWh; -2.54% for the April 2022 contract, to €71.748/MWh) helped accompany the downtrend. The lingering tension on the Ukrainian border (although there was no escalation) provided some support to far curve prices.

At the close, NBP ICE March 2022 prices dropped by 3.180 p/th day-on-day (-1.77%), to 176.490 p/th. TTF ICE March 2022 prices were down by €1.15 (-1.54%), closing at €73.762/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 23 euro cents (-0.44%), closing at €51.663/MWh.

The 5-day average continued to set strong resistance to TTF ICE March 2022 prices on Friday. Prices are weakening again this morning, probably under the pressure from hopes of an easing on the Ukrainian crisis. Indeed, Presidents Putin and Biden agreed this Monday to meet at a summit, proposed by their French counterpart Macron, on the condition that an invasion of Ukraine did not take place. The recovery in Norwegian supply (to 346 mm cm/day on average this morning) is also providing downward pressure. However, as already mentioned on Friday, the downside potential may be limited as both the technical levels (the 5-day Low and 20-day Low targets) and the fundamental levels (in particular the upper level of the spot coal switching range in power generation, currently around €66/MWh) could lend support.