Oil prices on the rise again

The price of Brent crude oil has risen by $2/b from yesterday morning and is now trading at $88.5/b, despite the further decline in US…

European gas prices weakened again on Friday, pressured by weak demand and comfortable supply. While Russian flows were stable, averaging 227 mm cm/day, Norwegian flows were up, to 325 mm cm/day on average, compared to 320 mm cm/day on Thursday. However, the rise in coal prices (+4.61% for API2 1st nearby prices, +4.01% for Cal 2023 prices) contributed to limit losses, particularly on far curve prices.

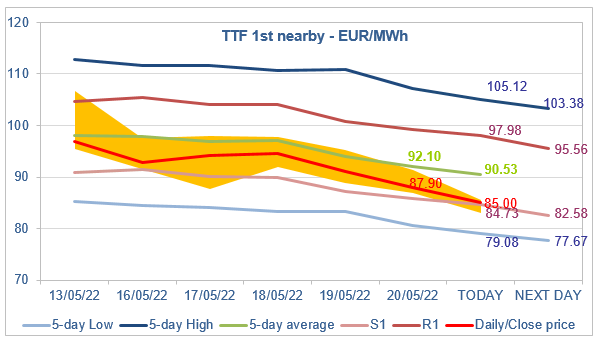

At the close, NBP ICE June 2022 prices dropped by 20.780 p/th (-12.31%), to 147.960 p/th, equivalent to €59.917/MWh. TTF ICE June 2022 prices were down by €3.12 (-3.43%), closing at €87.902/MWh. On the far curve, TTF ICE Cal 2023 prices dropped by 81 euro cents (-1.05%), closing at €75.708/MWh.

In Asia, JKM spot prices increased by 4.76%, to €70.024/MWh; July 2022 prices increased by 0.41%, to €70.521/MWh; August 2022 prices increased by 2.07%, to €75.206/MWh.

The rise in coal prices drove the coal switching range up. But, European power markets are currently comfortable enough to reduce the call to thermal generation. As a consequence, the equilibrium level for gas prices (from the perspective of power generation) should drop and settle around we can call the summer coal switching level (see the Gas & Coal Weekly Report published on Friday), which is currently around €75.27/MWh on the month-ahead. For the moment, TTF ICE June 2022 prices maintain their downtrend, inside a range whose the S1 level provides the support. In the absence of a major fundamental event, the summer coal switching level could be the target, knowing that Asia JKM prices should prevent prices from falling too much anyway.