Mixed signals

As the Fed chairman said during the week-end, the US economy is ready for a very strong recovery, but the economic outlook remains dependent on…

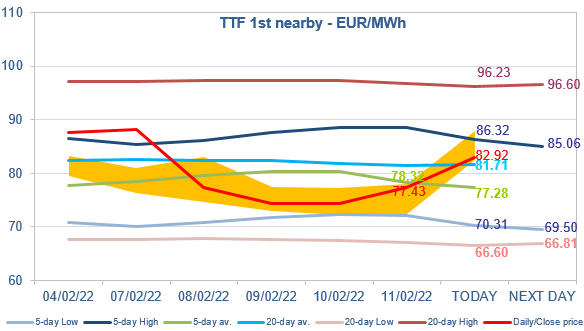

European gas prices rebounded overall on Friday, mainly supported by lower Russian supply (191 mm cm/day on average, compared to 196 mm cm/day on Thursday and 237 mm cm/day on Monday) as flows through Ukraine continued to weaken. On their side, Norwegian flows were up, averaging 333 mm cm/day, compared to 330 mm cm/day on Thursday. The trend in Asia JKM prices (-5.26% on the spot, to €71.070/MWh; -0.23% for the March 2022 contract, to €73.871/MWh; +4.28% for the April 2022 contract, to €77.750/MWh) tends to indicate that, while Europe should remain the market of choice for flexible LNG cargoes in February and March, this picture could change from April with Asian buyers increasing their bids. Increased military activity on the Ukrainian border also provided support, particularly for far curve prices.

At the close, NBP ICE March 2022 prices increased by 7.700 p/th day-on-day (+4.32%), to 185.860 p/th. TTF ICE March 2022 prices were up by €3.07 (+4.13%), closing at €77.426/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €2.40 (+4.65%), closing at €53.897/MWh.

TTF ICE March 2022 prices closed slightly below the 5-day average on Friday. But, with tensions escalating at the Ukrainian border over the week-end, they are breaking this resistance level this morning, rising towards the 5-day High. This 5-day High should set a stronger resistance, particularly as the levels of Asia JKM prices do not justify that European buyers continue to bid higher. However, if the geopolitical situation deteriorates further, a rise towards the 20-day High cannot be excluded.