Economic rebound threatened by the Indian variant and inflation

The rebound in new Covid cases in some Asian countries and in the UK is a threat for the current economic recovery. In the US,…

Crude prices remained elevated, at 82.2 $/b for ICE Brent front-month price, despite the SPR release announcement and a relatively neutral EIA weekly snapshot. Total crude inventories declined (accounting for the SPR release of last week) while distillate stocks declined further, likely due to a slower than anticipated ramp-up in US refining runs. Gasoline inventories also hovered around the lower end of the 5-year average, but draws should ease after Thanksgiving due to consumer hoarding. US demand remained very strong, at 21.8 mb/d for last week, at a seasonally all-time high.

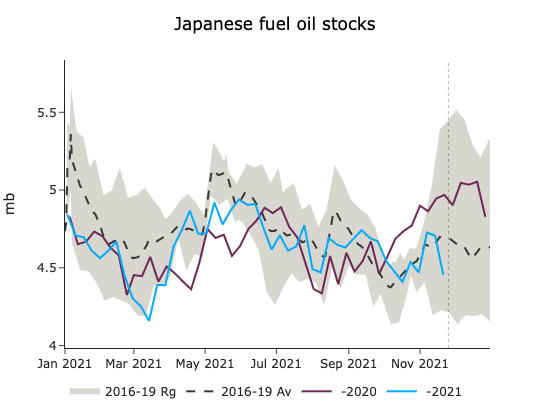

In Japan, crude stocks built by 3.2 mb while diesel stocks managed to stabilize at 8 mb. There is still no signs of winter planning seen in Japanese stocks which would lend support to the oil-to-gas switching theory. Diesel and fuel oil stocks are low and did not exhibit any material builds despite all Asian petroleum product prices incentivizing switching in the power sector.