Curve prices extended gains

European spot gas prices were up again overall yesterday, supported by an additional tightness on supply. Indeed, Norwegian flows dropped significantly yesterday to 150 mm…

European gas prices were up overall yesterday, supported by lower pipeline supply and resilient coal prices. Indeed, Russian supply dropped again yesterday, averaging 217 mm cm/day, compared to 225 mm cm/day on Tuesday. Norwegian flows dropped to 325 mm cm/day on average, compared to 334 mm cm/day on Tuesday, due to an unplanned outage at the Aasta Hansteen field.

At the close, NBP ICE May 2022 prices increased by 1.940 p/th day-on-day (+0.92%), to 213.090 p/th. TTF ICE May 2022 prices were up by €3.11 (+3.04%), closing at €105.324/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €3.19 (+3.98%), closing at €83.452/MWh.

In Asia, JKM spot prices dropped by 2.17%, to €91.891/MWh; May 2022 prices dropped by 0.66%, to €103.211/MWh.

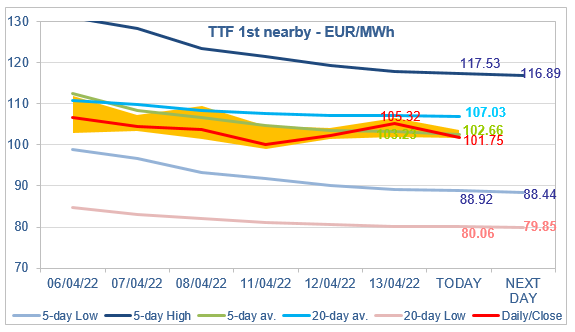

The maximum coal switching level was stable yesterday, around €98/MWh. Once again, this contributed to limit the downside potential for TTF ICE May 2022 prices. They rose above the 5-day average (currently at €102.66/MWh) but remained below the 20-day average (€107.03/MWh). As we said in our Gas & Coal Weekly Report published this morning, whether or not API2 1st nearby prices will break the resistance of the 1-Year High (they are nearing), this will give a first indication!