US crude production remains below 11 mb/d

ICE Brent crude oil gained a dollar, to 67.7 $/b at the prompt, supported by a relatively constructive EIA weekly report but also strengthening cracks…

European gas prices increased again yesterday, receiving additional support from lower Norwegian supply (down to 331 mm cm/day on average yesterday, compared to 349 mm cm/day on Tuesday, due to an unplanned outage at the Oseberg field), while Russian flows remained weak (slightly up to 185 mm cm/day on average, compared to 183 mm cm/day on Tuesday). The rise in Asia JKM prices (+8.39% on the spot, to €96.679/MWh; +4.15% for the February 2022 contract, to €103.122/MWh) helped accompany the bullish momentum.

Note that Indonesian authorities postponed the meeting scheduled yesterday with coal mining companies to discuss on the coal exports ban; no new time had been agreed.

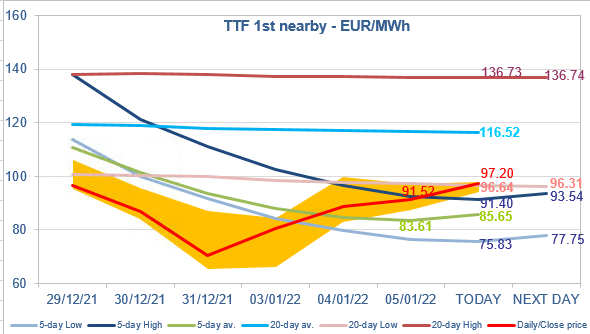

At the close, NBP ICE February 2022 prices increased by 6.880 p/th day-on-day (+3.18%), to 223.450 p/th. TTF ICE February 2022 prices were up by €2.78 (+3.13%), closing at €91.522/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.46 (+3.04%), closing at €49.455/MWh.

As expected, TTF ICE February 2022 prices traded during most of yesterday’s session in the zone around the 5-day High and the 20-day Low, before closing slightly below the first. They are increasing again this morning, around the 20-day Low. The “normalization” process (ie the gradual increase of prices inside the 20-day range) is therefore ongoing. This process is supported by the level of Asia JKM prices and the ban (still ongoing) on Indonesia coal exports.