Gas & Power Report: Mixed energy prices amidst a bustling environment

Gas & Power Podcast #32 In this weekly Gas & Power report, Julien Hoarau tells us about French nuclear availability and issues EDF encounters, impact…

European gas prices extended losses yesterday, still pressured by weak demand and strong LNG supply. The drop in coal prices (-4.37% for API2 1st nearby prices, -5.89% for Cal 2023 prices) provided additional downward pressure. On the pipeline supply side, Norwegian flows dropped to 311 mm cm/day on average yesterday, compared to 320 mm cm/day on Friday. Russian flows were almost stable, averaging 261 mm cm/day, compared to 260 mm cm/day on Friday.

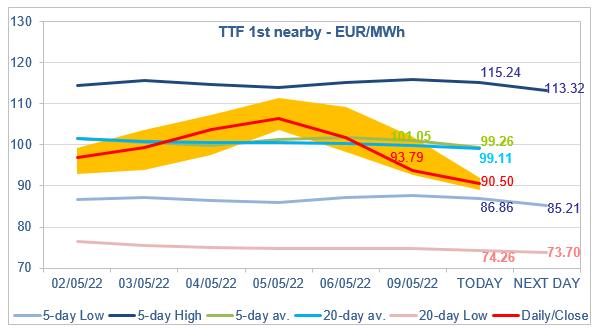

At the close, NBP ICE June 2022 prices dropped by 8.790 p/th (-6.39%), to 128.710 p/th. TTF ICE June 2022 prices were down by €7.92 (-7.79%), closing at €93.787/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €5.29 (-6.35%), closing at €78.052/MWh.

In Asia, JKM spot prices dropped by 13.69%, to €65.043/MWh; June 2022 prices dropped by 3.68%, to €74.854/MWh.

The drop in coal prices pulled the maximum coal switching level to 97.68/MWh yesterday (compared to 102.37/MWh on Friday). The next fundamental level is the average coal switching level, currently at 74.45 /MWh, and which is very close to the 20-day Low. Before they get there, TTF ICE June 2022 prices will have to break first the technical support of the 5-day Low. They seem on track as they are down again this morning. But as we have repeated several times, all of this remains conditional on two key fundamental factors: the continuation of a strong LNG supply in Europe and the continuation of Russian gas deliveries.