New all-time highs for EUA prices

EUA prices hit a new record high on Wednesday at €94.63/ton intraday for the Dec-22 contract with no fundamental driver at first glance. It should…

European gas prices were up again yesterday, supported by the additional rise in coal prices (+10.31% for API2 1st nearby prices; +8.72% for Cal 2023 prices). The rise in Norwegian flows (to 337 mm cm/day on average yesterday, compared to 327 mm cm/day on Tuesday) failed to calm the upward pressure. On their side, Russian flows remained stable, averaging 260 mm cm/day.

The rise in oil prices (+4.93% for Brent 1st nearby prices) after the European Commission proposed to phase out Russian oil imports by the end of 2022 provided additional support.

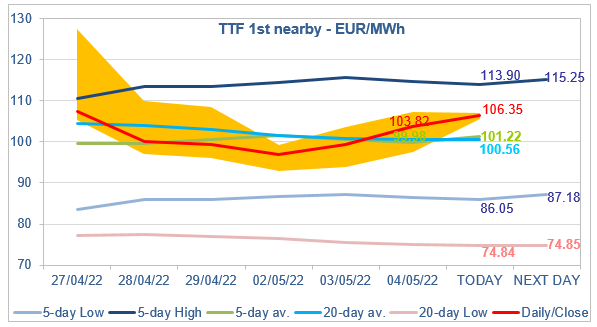

At the close, NBP ICE June 2022 prices increased by 3.030 p/th (+1.94%), to 159.200 p/th. TTF ICE June 2022 prices were up by €4.40 (+4.42%), closing at €103.821/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €5.40 (+6.96%), closing at €82.988/MWh.

In Asia, JKM 2022 prices increased by 1.33%, to €77.232/MWh, above the level of spot prices (€74.965/MWh).

The strong rise in coal prices pulled the maximum coal switching level to 99.44/MWh yesterday (up from 93.64/MWh on Tuesday), offering once again upside potential to TTF ICE June 2022 prices, which finally broke the resistance of the 5-day average and the 20-day average. Very close to the maximum coal switching level, these latter seem now to operate as support. In this context, a rise towards the 5-day High (113.90/MWh for today) cannot be excluded in the very short term.