Mixed signals

As the Fed chairman said during the week-end, the US economy is ready for a very strong recovery, but the economic outlook remains dependent on…

The statements of the central bankers meeting in Sintra, from the ECB or the Fed, are unambiguous: the priority is the fight against inflation. They are generally confident that a recession should be avoided, but warn that signs of economic slowdown do not distract them from their main short-term objective. Against this backdrop, equity markets continue to fall and so do yields, with the US 10-year back to just above 3%. The US dollar has also strengthened significantly, with the EUR/USD exchange rate plunging towards 1.0450.

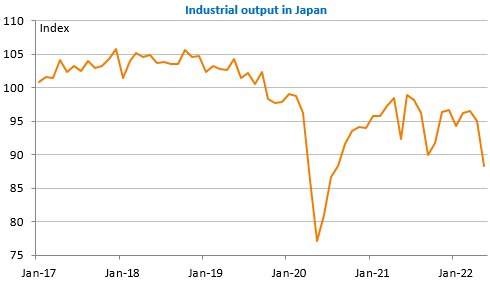

The Chinese markets are a bit of an exception, rising after the publication of better than expected purchasing managers’ indexes: 50.1 in the manufacturing sector and especially 54.7 in services, the highest level since May 2021, indicating a strong rebound in activity in June. Given the collapse of Japan’s industrial production in April (-1.5%) and May (-7.2% mom!), it is clear that China’s anti-covid measures have had serious repercussions on the production lines of its neighbours and elsewhere.

Many other figures have already been or will be published today: household consumption recovered a little in May in France (+0.7% mom) and in Germany (+0.6% for retail sales). But the effects of inflation will continue to be felt: the drop recorded in Germany (+8.2% yoy in June after +8.7%) will last only as long as temporary measures in transport this summer. Inflation has risen to 10% in Spain, 9.65% in Belgium and 6.5% in France. The trend is clearly upwards.

In the US, we will have the usual jobless claims and household consumption and income in May with the Fed’s favourite inflation measure: the core PCE deflator.