Rally in Atlantic gasoline markets

Crude prices remained supported to 71.8 $/b for ICE Brent prompt futures. As the EIA weekly release showed a seasonally average week, with stock draws in crude…

European gas prices dropped yesterday as the impact of the force majeure on the Sokhranivka entry point faded somewhat. But, physically, Russian flows through Ukraine at the Velke Kapusany entry point weakened further yesterday, averaging 67 mm cm/day, compared to 81 mm cm/day on Tuesday, driving total Russian flows to 236 mm cm/day on average, compared to 250 mm cm/day on Tuesday. On their side, Norwegian flows increased to 316 mm cm/day on average yesterday, compared to 306 mm cm/day on Tuesday.

The rise in coal prices (+5.24% for API2 1st nearby prices, +4.17% for Cal 2023 prices) helped limit losses on far curve prices.

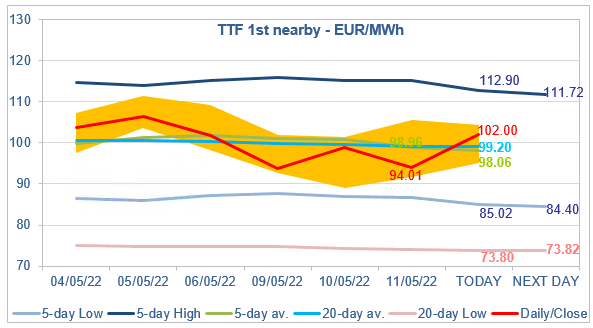

At the close, NBP ICE June 2022 prices dropped by 6.030 p/th (-4.14%), to 139.740 p/th. TTF ICE June 2022 prices were down by €4.79 (-4.85%), closing at €94.012/MWh. On the far curve, TTF ICE Cal 2023 prices dropped by 37 euro cents (-0.46%), closing at €79.201/MWh.

In Asia, JKM spot prices increased by 12.31%, to €70.435/MWh; June 2022 prices increased by 1.87%, to €75.882/MWh.

Russian flows through Ukraine are nominated lower again this morning, at 47 mm cm/day. Moreover, the rise in coal prices pulled the maximum coal switching level to €100.41/MWh yesterday, up from €96.35/MWh on Tuesday. The market seems to consider this to be an accumulation of bullish news and is pushing TTF ICE June 2022 prices higher this morning. Current fundamentals suggest the 5-day High target (€112.90/MWh for today) might be difficult to reach, but the intermediate target at €105.41/MWh seems quite attainable.