EU discusses possible embargo on Russian oil imports

Officially, nothing has been decided and some countries, starting with Germany, remain opposed to stopping oil imports from Russia because they have no immediate alternative. But the…

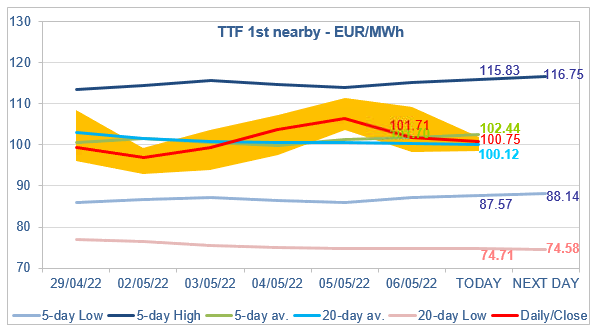

European spot gas prices dropped strongly on Friday, pressured by weak demand and ongoing strong LNG supply while pipeline flows remained stable (Norwegian flows at 320 mm cm/day on average, and Russian flows at 260 mm cm/day on average). The drop in curve prices was more moderate, particularly on the TTF, as concerns on the future of Russian supply and resilient coal prices lent support.

At the close, NBP ICE June 2022 prices dropped by 28.730 p/th (-17.28%), to 137.500 p/th. TTF ICE June 2022 prices were down by €4.80 (-4.51%), closing at €101.708/MWh. On the far curve, TTF ICE Cal 2023 prices were down by €2.03 (-2.37%), closing at €83.341/MWh.

In Asia, JKM spot prices dropped by 1.47%, to €75.363/MWh; June 2022 prices dropped by 0.58%, to €77.712/MWh.

The slight drop in coal prices was offset by higher EUA prices on Friday, maintaining the maximum coal switching level stable at 102.37/MWh. TTF ICE June 2022 prices closed slightly below this level on Friday, around the 5-day average. They are slightly down this morning, between the 20-day average and the 5-day average. This perfectly reflects the current balance of risks: the market does not feel secure enough to push June 2022 prices towards the 5-day Low (level at which TTF day-ahead prices were assessed on Friday, and even much lower on some other markets) and spot fundamentals are too comfortable to push these June prices to the 5-day High. A major fundamental event could obviously break this equilibrium.