Fall in European prices

European gas prices dropped yesterday, pressured by the expected rise in temperatures next week. The sharp drop in oil prices and the more moderate drop…

European gas prices took a breather after their strong rise of the previous session. The drop in coal prices (-3.34% for API2 1st nearby prices, -3.95% for Cal 2023 prices) also exerted downward pressure. For the moment, this decline in coal prices is essentially technical. But a more significant decline is possible if the global coal market ultimately turns out to be less tight than feared (see the Gas & Coal Weekly Report published on Friday).

On the pipeline supply side, Russian flows remained stable on Friday at 104 mm cm/day on average. On their side, Norwegian flows rebounded, averaging 311 mm cm/day, compared to 298 mm cm/day on Wednesday.

At the close, NBP ICE July 2022 prices dropped by 17.100 p/th (-9.15%), to 169.740 p/th, equivalent to €67.339/MWh. TTF ICE July 2022 prices were down by €4.842 (-3.63%), closing at €128.505/MWh. On the far curve, TTF ICE Cal 2023 prices dropped by €2.317 (-2.34%), closing at €96.865/MWh.

In Asia, JKM spot prices dropped by 0.96%, to €119.261/MWh; August 2022 prices dropped by 0.09%, to €119.930/MWh.

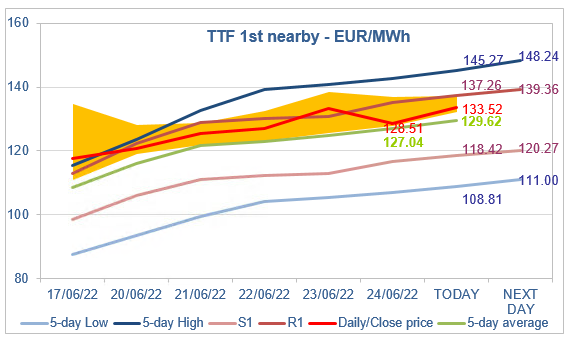

TTF 1st nearby prices did not manage to drop below the 5-day average on Friday (which would have paved the way for a drop towards the 20-day High, which stands at €126.08/MWh for today, and would have accelerated the “normalization” process). Prices are rebounding this morning. The trading range for today could be between the 5-day average and the R1 level. The “normalization” process requires prices to trade in the lower part of this range, but upside risks cannot be ignored.