A break before choosing

While the fighting in Ukraine is intensifying, financial markets seem to be calming down somewhat. Equity markets trimmed their losses in Europe yesterday, fell little…

European gas prices continued to weaken yesterday, pressured by forecasts of milder weather amid ongoing strong LNG supply. The announcement of a possible Putin-Biden summit pushed prices down early in the morning. But the downtrend slightly reversed later in the day after the Kremlin spokesperson said a call or meeting between the two presidents could be set up at any time, but there were no concrete plans yet for a summit. He added that tensions were growing, but a foreign ministers’ meeting was possible this week. On the pipeline supply side, Norwegian flows recovered to 344 mm cm/day on average yesterday, compared to 320 mm cm/day on Friday. Russian supply was lower, averaging 182 mm cm/day, compared to 186 mm cm/day on Friday.

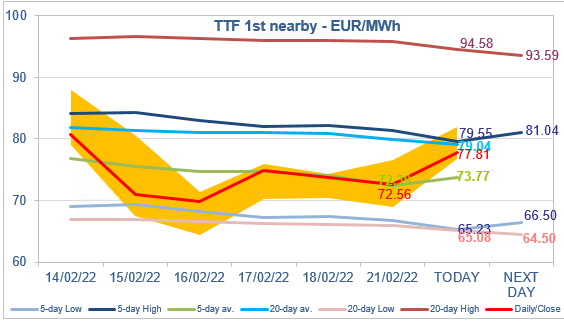

At the close, NBP ICE March 2022 prices dropped by 2.960 p/th day-on-day (-1.68%), to 173.530 p/th. TTF ICE March 2022 prices were down by €1.20 (-1.62%), closing at €72.564/MWh. On the far curve, TTF ICE Cal 2023 prices were down by 7 euro cents (-0.14%), closing at €51.591/MWh.

Yesterday, TTF ICE March 2022 prices were almost perfectly distributed around their 5-day average, reflecting the uncertainty of the market to choose a trend. They are up this morning, trading around the 20-day average and the 5-day High target, a move that can still be considered as arising from the (normal) market volatility. Therefore, these levels should set a resistance. But, obviously, any unfavorable development in the Ukrainian crisis could lead prices to break this resistance.