Gas & Power Report: The upward trend is running out of steam

Gas & Power Report: The upward trend is running out of steam December, 6 2024 Gas & Power November saw European gas and power prices…

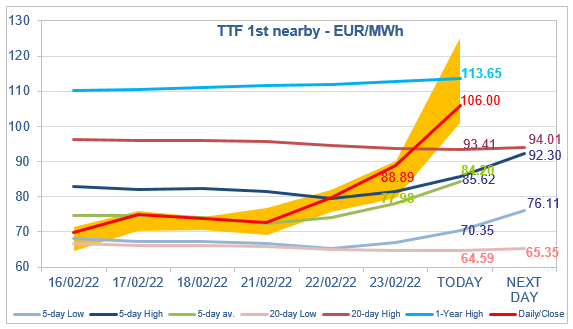

European gas prices continued to increase yesterday, still supported by rising tensions in Ukraine. At the close, NBP ICE March 2022 prices increased by 22.340 p/th day-on-day (+11.70%), to 213.330 p/th. TTF ICE March 2022 prices were up by €9.10 (+11.41%), closing at €88.891/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €5.60 (+9.81%), closing at €62.622/MWh.

But attention is obviously focused this morning on the Russian military offensive in Ukraine and the strikes in various places of the country. Yesterday, Russian gas flows through Ukraine increased to 35 mm cm/day (compared to 25 mm cm/day on Tuesday), driving total Russian flows to 204 mm cm/day (compared to 185 mm cm/day). There is no indication of supply interruption this morning, with even flows through Ukraine estimated to be still on the rise, probably because long term buyers are increasing their offtakes. However, panic buying are pushing prices sharply up. Is this justified? Yesterday, US officials said that even if Russia invaded Ukraine, the Biden administration was not expected to target Russia’s crude oil and refined fuel sector with sanctions cutting off trade, due to concerns about inflation and the harm it could do to its European allies, global oil markets and US consumers. The focus was on oil, but we can add gas in the picture. This suggests that, for the time being, the most likely scenario is that Russian volumes will continue to flow, the main sanction remaining the halt of the certification process of Nord Stream 2 (see our news released yesterday). In this central scenario, the European gas balance will remain tight, but prices will remain at levels that can be fundamentally justified: above the coal switching levels for sure, but below the most expensive gasoil switching levels (around €111/MWh currently on the spot). Note that the latter is close to the 1-Year High target (€113.65/MWh for today). Therefore, there are both technical and fundamental levels to prevent prices from skyrocketing further. And actually, TTF ICE March 2022 prices seem to find resistance around those levels. But this needs to be confirmed: on the one hand with financial participants taking their profits (it seems to be already the case), on the other hand with physical participants switching to oil products or cutting consumption. This reaction of the physical market is much more difficult to assess and forecast, but the behavior of Asian buyers could give us rapidly an indication.