Prices rallied following the invasion of Ukraine by Russia

European gas prices rallied yesterday following the invasion of Ukraine by Russia. At the close, NBP ICE March 2022 prices increased by 108.640 p/th day-on-day…

European gas prices rebounded yesterday, supported by cold weather and the US State Department decision to impose sanctions on a Russia-linked company and its work ship involved in finishing the Nord Stream 2 gas pipeline. The rise in Asia JKM January 2022 prices (+6.08%, to €109.455/MWh, while spot prices dropped slightly by 0.49% to €102.916/MWh) helped accompany the bullish momentum. On the spot pipeline supply side, Norwegian flows were almost stable yesterday, at 344 mm cm/day on average, compared to 343 mm cm/day on Monday. Russian supply was stable, averaging 288 mm cm/day.

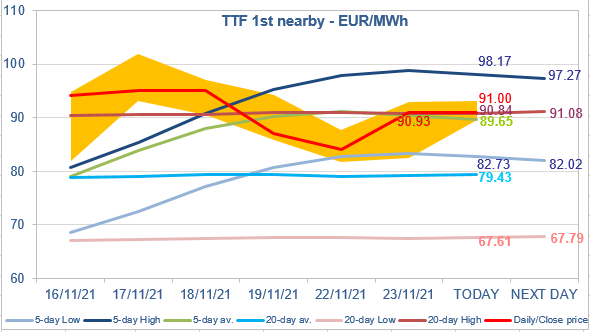

At the close, NBP ICE December 2021 prices increased by 17.880 p/th day-on-day (+8.47%), to 229.050 p/th. TTF ICE December 2021 prices were up by €6.91 (+8.22%) at the close, to €90.927/MWh. On the far curve, TTF Cal 2022 prices were up by €2.83 (+5.48%), closing at €54.377/MWh, with the spread against the coal parity price (€38.149/MWh, +3.41%) widening.

The upward move yesterday drove TTF ICE December 2021 prices to the 5-day average and the 20-day High levels, which opposed resistance. They are still resisting the bullish momentum this morning. As the Asia JKM price sent a mixed signal yesterday (utilities don’t seem to be ready to outbid for spot cargoes but they are incline to do so for January 2022 cargoes when power demand will rise significantly), TTF ICE December 2021 could stabilize around their current levels. But given the spread with JKM prices, the bias is upward.