Market anticipates ECB monetary tightening

Over the last two days, the German 10 year bond yield has increased by 7bp while the US 10 year is only up 3bp and…

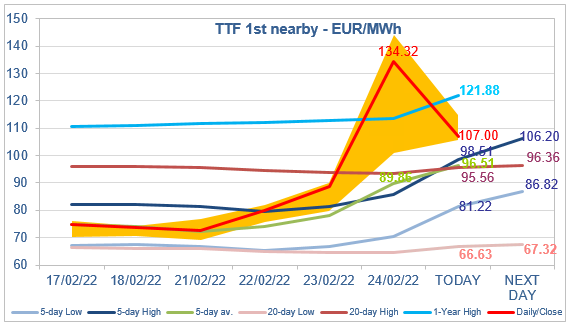

European gas prices rallied yesterday following the invasion of Ukraine by Russia. At the close, NBP ICE March 2022 prices increased by 108.640 p/th day-on-day (+50.93%), to 321.970 p/th. TTF ICE March 2022 prices were up by €45.42 (+51.10%), closing at €134.316/MWh. Note however that the rise in TTF day-ahead prices was lower (+32.81%, to €118.000/MWh). On the far curve, TTF ICE Cal 2023 prices were up by €15.17 (+24.22%), closing at €77.790/MWh.

In Asia, JKM spot prices increased by 33.65%, to €112.874/MWh; April 2022 prices increased by 29.12%, to €112.844/MWh.

This strong price increase was obviously fueled by panic buying and concerns about what could happen next. But, from the strict point of view of gas supply, there was no particular tension, and Russian flows even increased yesterday, averaging 226 mm cm/day (compared to 204 mm cm/day on Wednesday), mainly because of the rise in flows through Ukraine from 35 to 57 mm cm/day. As we said yesterday, for us, the most likely scenario is that Russian volumes will continue to flow, a scenario which is backed by the content of the sanctions decided for the moment by Europe and the US (well aware of the effect that an interruption in Russian oil and gas exports could have on already very high inflation levels) and Gazprom’s booking of transportation capacity through Ukraine yesterday. And even if military operations led for one reason or another to a cut in flows through Ukraine, Gazprom could still use its transportation capacity through Poland which is currently unused.

The market seems to digest all this information and TTF ICE March 2022 prices are falling this morning, probably pressured by profit taking by financial participants. It is interesting to notice that they are now trading below the 1-Year High target, but the latter is strongly up compared to its yesterday value, inflated by the rising trend and the market volatility. Signals sent by the physical market (discounted spot prices, lower Asia JKM prices, an estimated €120/MWh for the most expensive gasoil switching possibilities) can also explain the moderation of the bullish momentum. But this is just a moderation with very limited hopes of significant price declines in the short term.