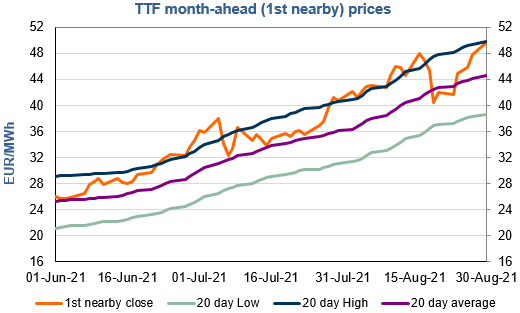

European prices up in anticipation of a ruling on Nord Stream 2

European gas prices increased strongly yesterday, continuing their technical rebound as many market participants preferred to close their short positions in anticipation of a German-court…