Crude oil prices sharply on the rise

Brent 1st-nearby prices have neared the key level of $70/b this morning. Expectations of higher oil output from OPEC+ producers and the potential comeback of…

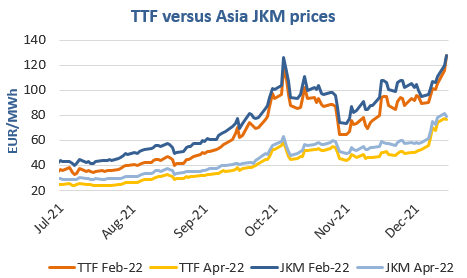

European gas prices maintained their strong uptrend yesterday, still supported by tight domestic fundamentals, while competition with Asia for LNG supply does not show yet strong and decisive signs of weakening. Indeed, Asia JKM prices were up by 1.15% on the spot, to €118.372/MWh, and by 6.33% for the February 2022 contract, to €127.566/MWh. On the spot pipeline supply side, Norwegian flows were slightly down yesterday, averaging 346 mm cm/day, compared to 349 mm cm/day on Monday. Russian supply was almost stable, at 280 mm cm/day on average, compared to 281 mm cm/day on average on Monday.

At the close, NBP ICE January 2022 prices increased by 28.860 p/th day-on-day (+9.80%), to 323.400 p/th. TTF ICE January 2022 prices were up by €12.22 (+10.52%) at the close, to €128.301/MWh. On the far curve, TTF Cal 2022 prices were up by €2.66 (+3.23%), closing at €85.014/MWh, with the spread against the coal parity price (€40.415/MWh, -0.50%) widening again significantly.

TTF ICE January 2022 prices closed again yesterday above the 5-day High. They are stabilizing this morning, to 128.00/MWh. The trend in Asia JKM prices yesterday sent mixed signals: Asian buyers are ready to leave some LNG cargoes to Europe on the spot (which is in line with the spot situation in Asia which is rather comfortable), but not for the whole winter as the weather risk is still present. But for the European bulls, these signals from Asia are indications that the uptrend is starting to be challenged, which could lead to less aggressive buying.