First decline in Chinese property prices since 2015

New home prices in China fell marginally in September for the first time since April 2015. A new property developer, Sinic, was also unable to meet…

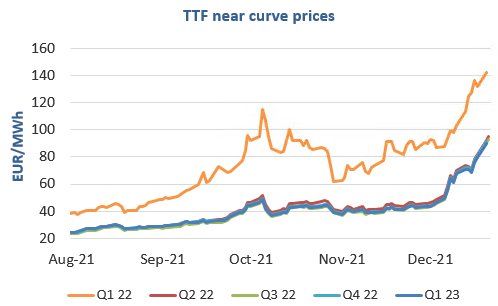

European gas prices increased strongly yesterday, mainly supported by lower Russian supply (down to 258 mm cm/day on average, compared to 281 mm cm/day on Friday, due to the drop in Mallnow flows through Poland). Norwegian flows were also down, to 342 mm cm/day on average, compared to 351 mm cm/day on Friday. Moreover, during the auctions of monthly transportation capacity held yesterday, Gazprom booked volumes (through Ukraine and Poland) which suggest its flows in January 2022 will not increase compared to their current levels. This triggered a strong increase in Cal 2022 prices. Note that Asia JKM prices were also up (+7.34% on the spot, to €127.719/MWh, +5.73% for the February 2022 contract, to €136.259/MWh), but remained below European prices.

At the close, NBP ICE January 2022 prices increased by 26.930 p/th day-on-day (+7.81%), to 371.830 p/th. TTF ICE January 2022 prices were up by €10.01 (+7.31%) at the close, to €146.926/MWh. On the far curve, TTF Cal 2022 prices were up by €10.50 (+11.23%), closing at €103.982/MWh.

TTF ICE January 2022 prices closed yesterday above the 5-day High. They are up again this morning, to €152.46/MWh, above the 5-day High for today (already known, at €149.23/MWh) but below the current estimate of the 5-day High for tomorrow (€154.57/MWh). This means that, for the bulls willing to buy today and resell tomorrow, the current price level is still attractive, as long as the fundamental trend remains bullish, which is the case. However, the lower levels of Asia JKM prices (which suggest higher LNG deliveries to Europe) could call for caution and limit the upside potential.