Macro & Oil Report: Markets continue to adjust to the new interest rate scenario

Markets continue to adjust to the new interest rate scenario Macro & Oil #90 Rates continue to rise as we await January’s US inflation figures…

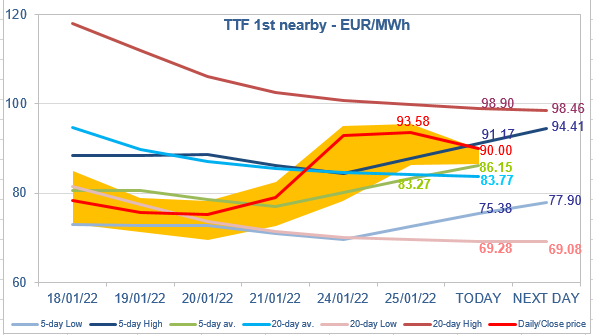

European gas prices increased slightly yesterday as the bullish impact of concerns on Russia-Ukraine tensions was partly offset by moderate demand, ongoing strong LNG sendouts and slight increase in spot pipeline flows. Indeed, Norwegian flows increased slightly yesterday, averaging 348 mm cm/day, compared to 346 mm cm/day on Monday. Russian supply was also slightly up, averaging 200 mm cm/day, compared to 198 mm cm/day on Monday. Note that Asia JKM prices (+13.94% on the spot, to €82.219/MWh; +3.45% for the March 2022 contract, to €78.532/MWh) sent bullish signals, showing that Asian buyers want to take from their European counterparts some of the available LNG cargos.

At the close, NBP ICE February 2022 prices increased by 0.620 p/th day-on-day (+0.28%), to 225.360 p/th. TTF ICE February 2022 prices were up by 58 euro cents (+0.63%), closing at €93.582/MWh. On the far curve, TTF ICE Cal 2023 prices were up by €1.42 (+2.91%), closing at €50.048/MWh.

TTF ICE February 2022 prices continued to trade above the 5-day High yesterday. But they are falling below this level this morning, probably pressured by profit taking from financial participants. Moreover, despite their strong rise yesterday, Asia JKM prices remain well below European prices, which means European buyers are not obliged to continue to overbid to maintain strong LNG inflows. However, amid geopolitical tensions over Ukraine, the short-term trend is bullish now, which limits the downside potential. In this context, the 5-day average and the 20-day average are strong support levels.